For beginners, it can seem like a good idea (and an exciting prospect) to buy a company that tells a good story to investors, even if it currently lacks a track record of revenue and profit. But as Peter Lynch said in One Up On Wall Street, 'Long shots almost never pay off.' Loss making companies can act like a sponge for capital - so investors should be cautious that they're not throwing good money after bad.

If this kind of company isn't your style, you like companies that generate revenue, and even earn profits, then you may well be interested in Trent (NSE:TRENT). Now this is not to say that the company presents the best investment opportunity around, but profitability is a key component to success in business.

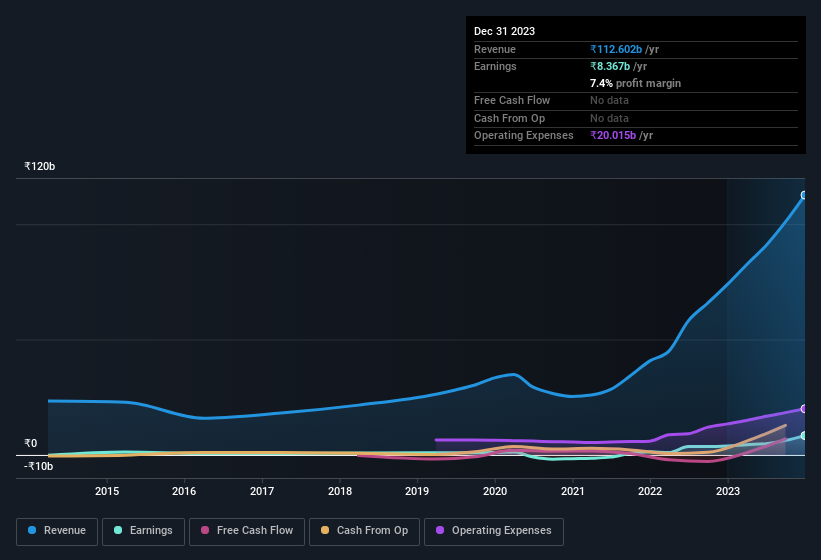

See our latest analysis for Trent

How Fast Is Trent Growing Its Earnings Per Share?

Trent has undergone a massive growth in earnings per share over the last three years. So much so that this three year growth rate wouldn't be a fair assessment of the company's future. As a result, we'll zoom in on growth over the last year, instead. Impressively, Trent's EPS catapulted from ₹11.00 to ₹23.54, over the last year. Year on year growth of 114% is certainly a sight to behold. The best case scenario? That the business has hit a true inflection point.

One way to double-check a company's growth is to look at how its revenue, and earnings before interest and tax (EBIT) margins are changing. While we note Trent achieved similar EBIT margins to last year, revenue grew by a solid 52% to ₹113b. That's progress.

The chart below shows how the company's bottom and top lines have progressed over time. For finer detail, click on the image.

Fortunately, we've got access to analyst forecasts of Trent's future profits. You can do your own forecasts without looking, or you can take a peek at what the professionals are predicting.

Are Trent Insiders Aligned With All Shareholders?

It's said that there's no smoke without fire. For investors, insider buying is often the smoke that indicates which stocks could set the market alight. This view is based on the possibility that stock purchases signal bullishness on behalf of the buyer. Of course, we can never be sure what insiders are thinking, we can only judge their actions.

We haven't seen any insiders selling Trent shares, in the last year. So it's definitely nice that company insider Wasi Ahmad bought ₹2.1m worth of shares at an average price of around ₹2,033. It seems that at least one insider is prepared to show the market there is potential within Trent.

Recent insider purchases of Trent stock is not the only way management has kept the interests of the general public shareholders in mind. Specifically, the CEO is paid quite reasonably for a company of this size. For companies with market capitalisations over ₹666b, like Trent, the median CEO pay is around ₹79m.

The Trent CEO received ₹54m in compensation for the year ending March 2023. That is actually below the median for CEO's of similarly sized companies. CEO remuneration levels are not the most important metric for investors, but when the pay is modest, that does support enhanced alignment between the CEO and the ordinary shareholders. It can also be a sign of good governance, more generally.

Should You Add Trent To Your Watchlist?

Trent's earnings have taken off in quite an impressive fashion. Not to mention the company's insiders have been adding to their portfolios and the CEO's remuneration policy looks to have had shareholders in mind seeing as it's quite modest for the company size. The strong EPS growth suggests Trent may be at an inflection point. For those attracted to fast growth, we'd suggest this stock merits monitoring. We don't want to rain on the parade too much, but we did also find 2 warning signs for Trent (1 shouldn't be ignored!) that you need to be mindful of.

Keen growth investors love to see insider buying. Thankfully, Trent isn't the only one. You can see a a curated list of Indian companies which have exhibited consistent growth accompanied by recent insider buying.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Valuation is complex, but we're here to simplify it.

Discover if Trent might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:TRENT

Trent

Engages in the retailing and trading of apparels, footwear, accessories, toys, games, and other products in India.

Exceptional growth potential with flawless balance sheet.

Similar Companies

Market Insights

Community Narratives