- India

- /

- Retail Distributors

- /

- NSEI:JMA

Jullundur Motor Agency (Delhi) Limited (NSE:JMA) Stock Rockets 34% But Many Are Still Ignoring The Company

Despite an already strong run, Jullundur Motor Agency (Delhi) Limited (NSE:JMA) shares have been powering on, with a gain of 34% in the last thirty days. Looking back a bit further, it's encouraging to see the stock is up 99% in the last year.

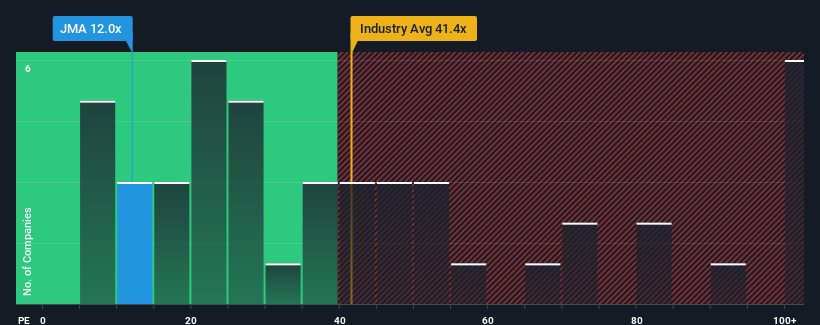

In spite of the firm bounce in price, Jullundur Motor Agency (Delhi)'s price-to-earnings (or "P/E") ratio of 12x might still make it look like a strong buy right now compared to the market in India, where around half of the companies have P/E ratios above 32x and even P/E's above 60x are quite common. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so limited.

For instance, Jullundur Motor Agency (Delhi)'s receding earnings in recent times would have to be some food for thought. One possibility is that the P/E is low because investors think the company won't do enough to avoid underperforming the broader market in the near future. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

View our latest analysis for Jullundur Motor Agency (Delhi)

What Are Growth Metrics Telling Us About The Low P/E?

The only time you'd be truly comfortable seeing a P/E as depressed as Jullundur Motor Agency (Delhi)'s is when the company's growth is on track to lag the market decidedly.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 8.8%. However, a few very strong years before that means that it was still able to grow EPS by an impressive 93% in total over the last three years. So we can start by confirming that the company has generally done a very good job of growing earnings over that time, even though it had some hiccups along the way.

Weighing that recent medium-term earnings trajectory against the broader market's one-year forecast for expansion of 24% shows it's about the same on an annualised basis.

In light of this, it's peculiar that Jullundur Motor Agency (Delhi)'s P/E sits below the majority of other companies. It may be that most investors are not convinced the company can maintain recent growth rates.

The Final Word

Jullundur Motor Agency (Delhi)'s recent share price jump still sees its P/E sitting firmly flat on the ground. Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've established that Jullundur Motor Agency (Delhi) currently trades on a lower than expected P/E since its recent three-year growth is in line with the wider market forecast. There could be some unobserved threats to earnings preventing the P/E ratio from matching the company's performance. It appears some are indeed anticipating earnings instability, because the persistence of these recent medium-term conditions should normally provide more support to the share price.

Plus, you should also learn about these 3 warning signs we've spotted with Jullundur Motor Agency (Delhi) (including 1 which doesn't sit too well with us).

You might be able to find a better investment than Jullundur Motor Agency (Delhi). If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:JMA

Jullundur Motor Agency (Delhi)

Trades and distributes automobile parts, accessories, and petroleum products primarily in India.

Flawless balance sheet average dividend payer.

Market Insights

Community Narratives