Advertisement

- India

- /

- Real Estate

- /

- NSEI:AJMERA

Market Might Still Lack Some Conviction On Ajmera Realty & Infra India Limited (NSE:AJMERA) Even After 27% Share Price Boost

Despite an already strong run, Ajmera Realty & Infra India Limited (NSE:AJMERA) shares have been powering on, with a gain of 27% in the last thirty days. The annual gain comes to 176% following the latest surge, making investors sit up and take notice.

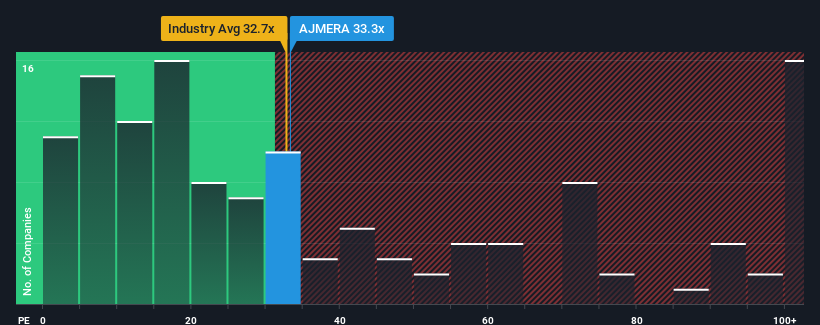

Although its price has surged higher, there still wouldn't be many who think Ajmera Realty & Infra India's price-to-earnings (or "P/E") ratio of 33.3x is worth a mention when the median P/E in India is similar at about 31x. While this might not raise any eyebrows, if the P/E ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

Earnings have risen firmly for Ajmera Realty & Infra India recently, which is pleasing to see. It might be that many expect the respectable earnings performance to wane, which has kept the P/E from rising. If that doesn't eventuate, then existing shareholders probably aren't too pessimistic about the future direction of the share price.

View our latest analysis for Ajmera Realty & Infra India

Is There Some Growth For Ajmera Realty & Infra India?

In order to justify its P/E ratio, Ajmera Realty & Infra India would need to produce growth that's similar to the market.

Retrospectively, the last year delivered an exceptional 26% gain to the company's bottom line. The strong recent performance means it was also able to grow EPS by 310% in total over the last three years. Therefore, it's fair to say the earnings growth recently has been superb for the company.

Weighing that recent medium-term earnings trajectory against the broader market's one-year forecast for expansion of 24% shows it's noticeably more attractive on an annualised basis.

In light of this, it's curious that Ajmera Realty & Infra India's P/E sits in line with the majority of other companies. It may be that most investors are not convinced the company can maintain its recent growth rates.

The Bottom Line On Ajmera Realty & Infra India's P/E

Its shares have lifted substantially and now Ajmera Realty & Infra India's P/E is also back up to the market median. Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that Ajmera Realty & Infra India currently trades on a lower than expected P/E since its recent three-year growth is higher than the wider market forecast. There could be some unobserved threats to earnings preventing the P/E ratio from matching this positive performance. At least the risk of a price drop looks to be subdued if recent medium-term earnings trends continue, but investors seem to think future earnings could see some volatility.

Don't forget that there may be other risks. For instance, we've identified 3 warning signs for Ajmera Realty & Infra India (2 are concerning) you should be aware of.

If these risks are making you reconsider your opinion on Ajmera Realty & Infra India, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:AJMERA

Ajmera Realty & Infra India

Engages in the real estate development business in India.

Solid track record with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Most Undervalued of the Magnificent 7

Fair Value US$237.43|37.8% undervalued

IN

Community Contributor

PVA TePla's New Strategy Aims for 22% Revenue Growth in Semiconductor Recovery

Fair Value €19.19|20.8% undervalued

MI

Community Contributor