Zydus Lifesciences' (NSE:ZYDUSLIFE) Upcoming Dividend Will Be Larger Than Last Year's

Zydus Lifesciences Limited (NSE:ZYDUSLIFE) will increase its dividend from last year's comparable payment on the 10th of September to ₹6.00. The payment will take the dividend yield to 1.1%, which is in line with the average for the industry.

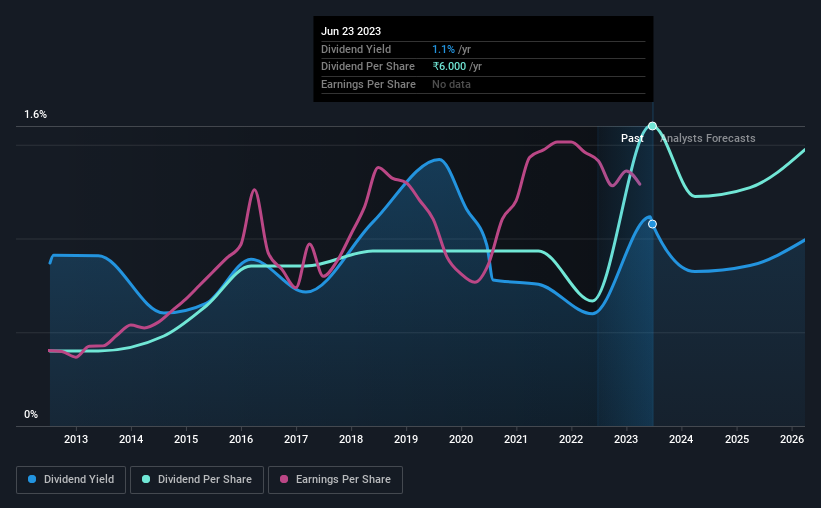

View our latest analysis for Zydus Lifesciences

Zydus Lifesciences' Payment Has Solid Earnings Coverage

Solid dividend yields are great, but they only really help us if the payment is sustainable. However, prior to this announcement, Zydus Lifesciences' dividend was comfortably covered by both cash flow and earnings. As a result, a large proportion of what it earned was being reinvested back into the business.

Over the next year, EPS is forecast to expand by 56.6%. If the dividend continues along recent trends, we estimate the payout ratio will be 21%, which is in the range that makes us comfortable with the sustainability of the dividend.

Dividend Volatility

The company has a long dividend track record, but it doesn't look great with cuts in the past. Since 2013, the annual payment back then was ₹1.50, compared to the most recent full-year payment of ₹6.00. This implies that the company grew its distributions at a yearly rate of about 15% over that duration. Dividends have grown rapidly over this time, but with cuts in the past we are not certain that this stock will be a reliable source of income in the future.

Dividend Growth May Be Hard To Achieve

Growing earnings per share could be a mitigating factor when considering the past fluctuations in the dividend. Earnings have grown at around 2.1% a year for the past five years, which isn't massive but still better than seeing them shrink. Earnings growth is slow, but on the plus side, the dividend payout ratio is low and dividends could grow faster than earnings, if the company decides to increase its payout ratio.

In Summary

Overall, it's great to see the dividend being raised and that it is still in a sustainable range. The payout ratio looks good, but unfortunately the company's dividend track record isn't stellar. This looks like it could be a good dividend stock going forward, but we would note that the payout ratio has been at higher levels in the past so it could happen again.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. As an example, we've identified 1 warning sign for Zydus Lifesciences that you should be aware of before investing. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

Valuation is complex, but we're here to simplify it.

Discover if Zydus Lifesciences might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:ZYDUSLIFE

Zydus Lifesciences

Engages in the research, development, production, marketing, distribution, and sale of pharmaceutical products in India, the United States, and internationally.

Flawless balance sheet with solid track record and pays a dividend.