Advertisement

Statutory Earnings May Not Be The Best Way To Understand Wanbury's (NSE:WANBURY) True Position

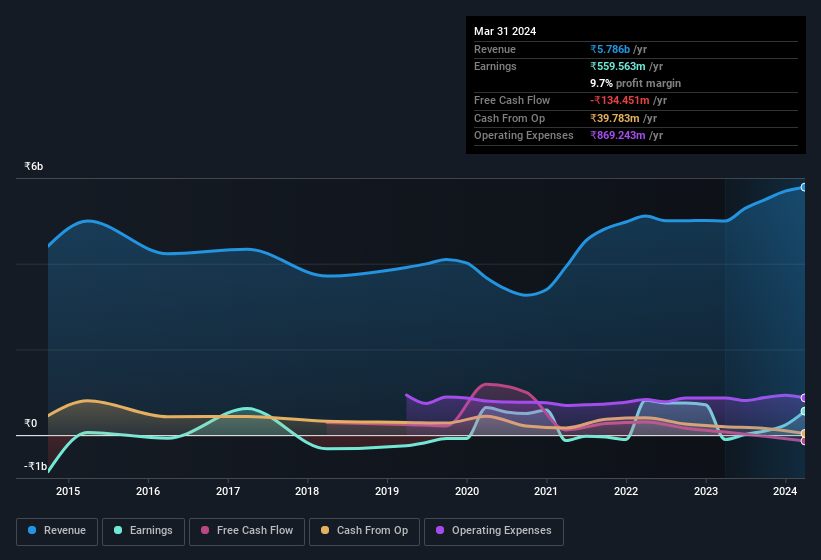

Wanbury Limited's (NSE:WANBURY) stock rose after it released a robust earnings report. Despite the strong profit numbers, we believe that there are some deeper issues which investors should look into.

View our latest analysis for Wanbury

Examining Cashflow Against Wanbury's Earnings

In high finance, the key ratio used to measure how well a company converts reported profits into free cash flow (FCF) is the accrual ratio (from cashflow). The accrual ratio subtracts the FCF from the profit for a given period, and divides the result by the average operating assets of the company over that time. You could think of the accrual ratio from cashflow as the 'non-FCF profit ratio'.

As a result, a negative accrual ratio is a positive for the company, and a positive accrual ratio is a negative. While it's not a problem to have a positive accrual ratio, indicating a certain level of non-cash profits, a high accrual ratio is arguably a bad thing, because it indicates paper profits are not matched by cash flow. Notably, there is some academic evidence that suggests that a high accrual ratio is a bad sign for near-term profits, generally speaking.

For the year to March 2024, Wanbury had an accrual ratio of 0.70. Statistically speaking, that's a real negative for future earnings. To wit, the company did not generate one whit of free cashflow in that time. Even though it reported a profit of ₹559.6m, a look at free cash flow indicates it actually burnt through ₹134m in the last year. We saw that FCF was ₹72m a year ago though, so Wanbury has at least been able to generate positive FCF in the past. However, that's not all there is to consider. The accrual ratio is reflecting the impact of unusual items on statutory profit, at least in part. One positive for Wanbury shareholders is that it's accrual ratio was significantly better last year, providing reason to believe that it may return to stronger cash conversion in the future. As a result, some shareholders may be looking for stronger cash conversion in the current year.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Wanbury.

The Impact Of Unusual Items On Profit

The fact that the company had unusual items boosting profit by ₹256m, in the last year, probably goes some way to explain why its accrual ratio was so weak. While we like to see profit increases, we tend to be a little more cautious when unusual items have made a big contribution. When we analysed the vast majority of listed companies worldwide, we found that significant unusual items are often not repeated. And, after all, that's exactly what the accounting terminology implies. We can see that Wanbury's positive unusual items were quite significant relative to its profit in the year to March 2024. All else being equal, this would likely have the effect of making the statutory profit a poor guide to underlying earnings power.

Our Take On Wanbury's Profit Performance

Summing up, Wanbury received a nice boost to profit from unusual items, but could not match its paper profit with free cash flow. On reflection, the above-mentioned factors give us the strong impression that Wanbury'sunderlying earnings power is not as good as it might seem, based on the statutory profit numbers. If you want to do dive deeper into Wanbury, you'd also look into what risks it is currently facing. For example, Wanbury has 4 warning signs (and 2 which are a bit unpleasant) we think you should know about.

In this article we've looked at a number of factors that can impair the utility of profit numbers, and we've come away cautious. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks with high insider ownership.

Valuation is complex, but we're here to simplify it.

Discover if Wanbury might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:WANBURY

Wanbury

Manufactures and sells formulations and active pharmaceutical ingredients (API) in India and internationally.

Proven track record low.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.7% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|87.9% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|20.5% undervalued

CH

Community Contributor