Advertisement

Syncom Formulations (India) Limited's (NSE:SYNCOMF) 27% Price Boost Is Out Of Tune With Earnings

Despite an already strong run, Syncom Formulations (India) Limited (NSE:SYNCOMF) shares have been powering on, with a gain of 27% in the last thirty days. Looking back a bit further, it's encouraging to see the stock is up 64% in the last year.

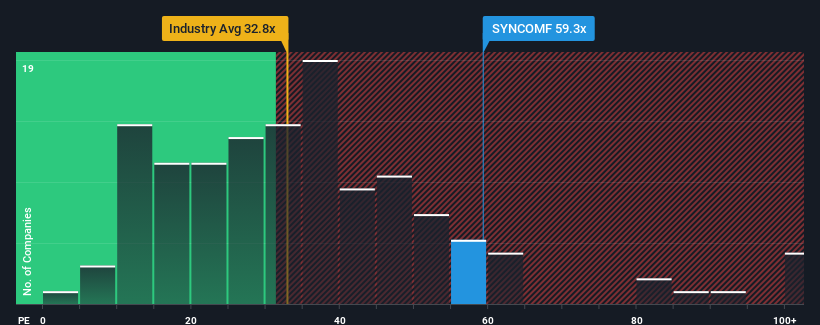

Following the firm bounce in price, Syncom Formulations (India) may be sending very bearish signals at the moment with a price-to-earnings (or "P/E") ratio of 59.3x, since almost half of all companies in India have P/E ratios under 29x and even P/E's lower than 16x are not unusual. However, the P/E might be quite high for a reason and it requires further investigation to determine if it's justified.

Recent times have been quite advantageous for Syncom Formulations (India) as its earnings have been rising very briskly. The P/E is probably high because investors think this strong earnings growth will be enough to outperform the broader market in the near future. If not, then existing shareholders might be a little nervous about the viability of the share price.

Check out our latest analysis for Syncom Formulations (India)

What Are Growth Metrics Telling Us About The High P/E?

Syncom Formulations (India)'s P/E ratio would be typical for a company that's expected to deliver very strong growth, and importantly, perform much better than the market.

If we review the last year of earnings growth, the company posted a terrific increase of 38%. Still, EPS has barely risen at all from three years ago in total, which is not ideal. Therefore, it's fair to say that earnings growth has been inconsistent recently for the company.

Weighing that medium-term earnings trajectory against the broader market's one-year forecast for expansion of 26% shows it's an unpleasant look.

In light of this, it's alarming that Syncom Formulations (India)'s P/E sits above the majority of other companies. It seems most investors are ignoring the recent poor growth rate and are hoping for a turnaround in the company's business prospects. There's a very good chance existing shareholders are setting themselves up for future disappointment if the P/E falls to levels more in line with the recent negative growth rates.

The Key Takeaway

Shares in Syncom Formulations (India) have built up some good momentum lately, which has really inflated its P/E. It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

Our examination of Syncom Formulations (India) revealed its shrinking earnings over the medium-term aren't impacting its high P/E anywhere near as much as we would have predicted, given the market is set to grow. Right now we are increasingly uncomfortable with the high P/E as this earnings performance is highly unlikely to support such positive sentiment for long. If recent medium-term earnings trends continue, it will place shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

You should always think about risks. Case in point, we've spotted 1 warning sign for Syncom Formulations (India) you should be aware of.

It's important to make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:SYNCOMF

Syncom Formulations (India)

Manufactures, markets, and sells pharmaceutical formulation products in India and internationally.

Flawless balance sheet with solid track record.

Market Insights

Advertisement

Weekly Picks

WO

woodworthfund on MGP Ingredients ·

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Fair Value:US$4034.1% undervalued

18 followersusers have followed this narrative

1 commentusers have commented on this narrative

4 likesusers have liked this narrative

DO

Double_Bubbler on Vertical Aerospace ·

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Fair Value:US$6090.0% undervalued

21 followersusers have followed this narrative

2 commentsusers have commented on this narrative

17 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8142.8% undervalued

41 followersusers have followed this narrative

3 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

MH

mhbb on Mastersystem Infotama ·

Mastersystem Infotama will achieve 18.9% revenue growth as fair value hits IDR1,650

Fair Value:Rp1.63k13.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Procter & Gamble ·

Insiders Sell, Investors Watch: What’s Going On at PG?

Fair Value:US$1506.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CW

Cwburton on Verano Holdings ·

Waiting for the Inevitable

Fair Value:CA$5.5278.8% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

119 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3926.6% undervalued

962 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8684.3% undervalued

77 followersusers have followed this narrative

8 commentsusers have commented on this narrative

21 likesusers have liked this narrative

Trending Discussion

OI

OilStates on Oil States International ·

This article is overall well written. However, to correct a few points and to highlight a few additional points: -The shift towards more stable long-cycle offshore and international projects does not increase volatility or exposure to short-cycle markets, quite the opposite. Offshore projects have a much longer investment cycle, duration, and low volatility given these are multi-decade assets. -The article notes a lack of exposure to renewables. Oil States has applied decades of experience in technologies for traditional oil & gas technologies into the renewables sector including transfer of fixed and floating offshore platform technologies into offshore wind, downhole perforating and well completions technologies into geothermal, along with over 50+ renewables projects completed. We are supportive of a broad energy mix, yet to meet growing global energy demand requires both traditional as well as lower carbon resources. Both elements as well as other industrial product orders continue to contribute to Oil States decade-high backlog, which provides significant future revenue visibility. -One of the main storylines not captured here is cash flow generation. 75% of Company revenues (up from 51% in 2022) now come from offshore and international work, which provides good margins. With the strength of the Offshore Manufactured Products business segment, the high-grading of U.S. domestic land activities to focus on higher margin business lines, free cash flow (a non-GAAP metric) has grown significantly ($70 million in free cash flow on a TTM basis as of Sept. 30, 2025). This is quite high for a Company at this market cap, which results in a higher free cash flow yield vs. peers. -Free cash is being used to repurchase shares, to pay down debt (nearing net-debt zero), and to increase returns to stockholders. More detail can be found in our latest investor presentation here: https://ir.oilstatesintl.com/events-and-presentations/default.aspx

0

|0