Advertisement

Things Look Grim For Entertainment Network (India) Limited (NSE:ENIL) After Today's Downgrade

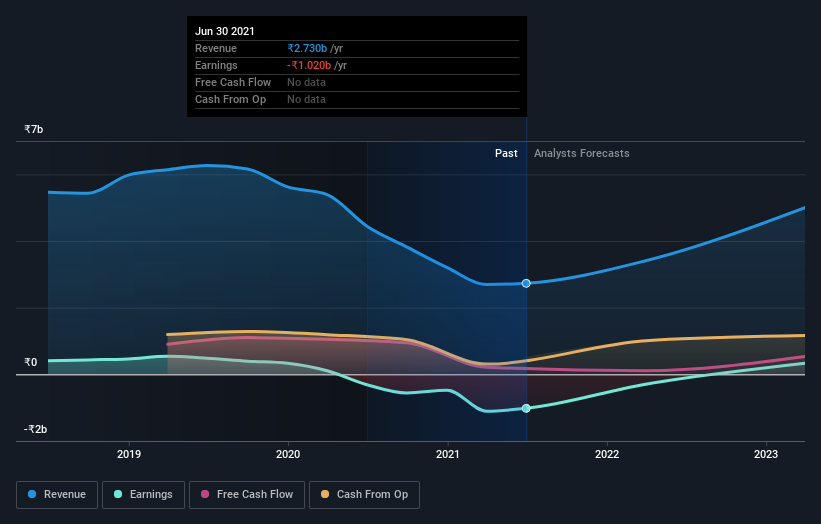

The latest analyst coverage could presage a bad day for Entertainment Network (India) Limited (NSE:ENIL), with the analysts making across-the-board cuts to their statutory estimates that might leave shareholders a little shell-shocked. Revenue and earnings per share (EPS) forecasts were both revised downwards, with the analysts seeing grey clouds on the horizon.

Following the downgrade, the most recent consensus for Entertainment Network (India) from its three analysts is for revenues of ₹3.4b in 2022 which, if met, would be a major 25% increase on its sales over the past 12 months. The loss per share is anticipated to greatly reduce in the near future, narrowing 71% to ₹6.20. Yet before this consensus update, the analysts had been forecasting revenues of ₹3.9b and losses of ₹1.97 per share in 2022. Ergo, there's been a clear change in sentiment, with the analysts administering a notable cut to this year's revenue estimates, while at the same time increasing their loss per share forecasts.

See our latest analysis for Entertainment Network (India)

Of course, another way to look at these forecasts is to place them into context against the industry itself. One thing stands out from these estimates, which is that Entertainment Network (India) is forecast to grow faster in the future than it has in the past, with revenues expected to display 34% annualised growth until the end of 2022. If achieved, this would be a much better result than the 7.5% annual decline over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in the industry are forecast to see their revenue grow 14% per year. So it looks like Entertainment Network (India) is expected to grow faster than its competitors, at least for a while.

The Bottom Line

The most important thing to take away is that analysts increased their loss per share estimates for this year. Unfortunately, analysts also downgraded their revenue estimates, although our data indicates revenues are expected to perform better than the wider market. Given the serious cut to this year's outlook, it's clear that analysts have turned more bearish on Entertainment Network (India), and we wouldn't blame shareholders for feeling a little more cautious themselves.

Still, the long-term prospects of the business are much more relevant than next year's earnings. At Simply Wall St, we have a full range of analyst estimates for Entertainment Network (India) going out to 2023, and you can see them free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

If you’re looking to trade Entertainment Network (India), open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Entertainment Network (India) might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NSEI:ENIL

Entertainment Network (India)

Together with its subsidiary, operates FM radio broadcasting stations in India and internationally.

6 star dividend payer with mediocre balance sheet.

Market Insights

Advertisement

Community Narratives

100% Patient Improvement in trial puts this $16M Biotech on the radar

Fair Value US$5.30|69.8% undervalued

JO

Community Contributor

Exxon Mobil's 17.5% Upside Promises Industry-Leading Returns in Energy Transition

Fair Value US$132.00|15.0% undervalued

HE

Community Contributor

NHC Analysis: Quality at a Good Price. A Golden Opportunity?

Fair Value US$179.80|36.1% undervalued

DA

Community Contributor

Product Refresh And Global Expansion Will Empower Future Market Leadership

Fair Value US$202.60|21.1% undervalued

AN

Based on Analyst Price Targets