Risks Still Elevated At These Prices As Thirumalai Chemicals Limited (NSE:TIRUMALCHM) Shares Dive 25%

Thirumalai Chemicals Limited (NSE:TIRUMALCHM) shareholders that were waiting for something to happen have been dealt a blow with a 25% share price drop in the last month. To make matters worse, the recent drop has wiped out a year's worth of gains with the share price now back where it started a year ago.

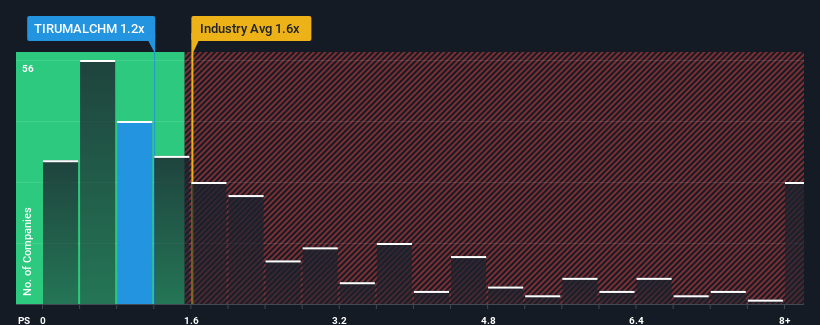

Although its price has dipped substantially, it's still not a stretch to say that Thirumalai Chemicals' price-to-sales (or "P/S") ratio of 1.2x right now seems quite "middle-of-the-road" compared to the Chemicals industry in India, where the median P/S ratio is around 1.6x. While this might not raise any eyebrows, if the P/S ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

See our latest analysis for Thirumalai Chemicals

How Has Thirumalai Chemicals Performed Recently?

The recent revenue growth at Thirumalai Chemicals would have to be considered satisfactory if not spectacular. Perhaps the expectation moving forward is that the revenue growth will track in line with the wider industry for the near term, which has kept the P/S subdued. If not, then at least existing shareholders probably aren't too pessimistic about the future direction of the share price.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on Thirumalai Chemicals will help you shine a light on its historical performance.Do Revenue Forecasts Match The P/S Ratio?

In order to justify its P/S ratio, Thirumalai Chemicals would need to produce growth that's similar to the industry.

Retrospectively, the last year delivered a decent 3.3% gain to the company's revenues. Revenue has also lifted 14% in aggregate from three years ago, partly thanks to the last 12 months of growth. So we can start by confirming that the company has actually done a good job of growing revenue over that time.

This is in contrast to the rest of the industry, which is expected to grow by 15% over the next year, materially higher than the company's recent medium-term annualised growth rates.

With this in mind, we find it intriguing that Thirumalai Chemicals' P/S is comparable to that of its industry peers. It seems most investors are ignoring the fairly limited recent growth rates and are willing to pay up for exposure to the stock. Maintaining these prices will be difficult to achieve as a continuation of recent revenue trends is likely to weigh down the shares eventually.

What Does Thirumalai Chemicals' P/S Mean For Investors?

With its share price dropping off a cliff, the P/S for Thirumalai Chemicals looks to be in line with the rest of the Chemicals industry. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

We've established that Thirumalai Chemicals' average P/S is a bit surprising since its recent three-year growth is lower than the wider industry forecast. Right now we are uncomfortable with the P/S as this revenue performance isn't likely to support a more positive sentiment for long. Unless the recent medium-term conditions improve, it's hard to accept the current share price as fair value.

Plus, you should also learn about these 3 warning signs we've spotted with Thirumalai Chemicals.

If these risks are making you reconsider your opinion on Thirumalai Chemicals, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Thirumalai Chemicals might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:TIRUMALCHM

Thirumalai Chemicals

Manufactures and sells organic chemicals in India and internationally.

Low and slightly overvalued.

Similar Companies

Market Insights

Community Narratives