Advertisement

Tata Chemicals Limited's (NSE:TATACHEM) Stock is Soaring But Financials Seem Inconsistent: Will The Uptrend Continue?

Most readers would already be aware that Tata Chemicals' (NSE:TATACHEM) stock increased significantly by 51% over the past three months. However, we decided to pay attention to the company's fundamentals which don't appear to give a clear sign about the company's financial health. Particularly, we will be paying attention to Tata Chemicals' ROE today.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. In other words, it is a profitability ratio which measures the rate of return on the capital provided by the company's shareholders.

Check out our latest analysis for Tata Chemicals

How Is ROE Calculated?

Return on equity can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Tata Chemicals is:

4.3% = ₹6.0b ÷ ₹139b (Based on the trailing twelve months to December 2020).

The 'return' is the income the business earned over the last year. That means that for every ₹1 worth of shareholders' equity, the company generated ₹0.04 in profit.

Why Is ROE Important For Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

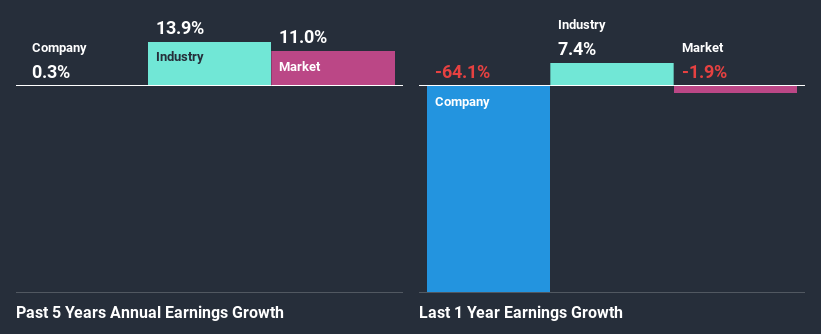

A Side By Side comparison of Tata Chemicals' Earnings Growth And 4.3% ROE

It is hard to argue that Tata Chemicals' ROE is much good in and of itself. Even when compared to the industry average of 13%, the ROE figure is pretty disappointing. Hence, the flat earnings seen by Tata Chemicals over the past five years could probably be the result of it having a lower ROE.

Next, on comparing with the industry net income growth, we found that Tata Chemicals' reported growth was lower than the industry growth of 14% in the same period, which is not something we like to see.

Earnings growth is an important metric to consider when valuing a stock. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). Doing so will help them establish if the stock's future looks promising or ominous. Is Tata Chemicals fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is Tata Chemicals Efficiently Re-investing Its Profits?

Despite having a normal three-year median payout ratio of 34% (implying that the company keeps 66% of its income) over the last three years, Tata Chemicals has seen a negligible amount of growth in earnings as we saw above. So there might be other factors at play here which could potentially be hampering growth. For example, the business has faced some headwinds.

In addition, Tata Chemicals has been paying dividends over a period of at least ten years suggesting that keeping up dividend payments is way more important to the management even if it comes at the cost of business growth. Our latest analyst data shows that the future payout ratio of the company over the next three years is expected to be approximately 32%. Regardless, the future ROE for Tata Chemicals is predicted to rise to 7.2% despite there being not much change expected in its payout ratio.

Conclusion

In total, we're a bit ambivalent about Tata Chemicals' performance. While the company does have a high rate of reinvestment, the low ROE means that all that reinvestment is not reaping any benefit to its investors, and moreover, its having a negative impact on the earnings growth. With that said, the latest industry analyst forecasts reveal that the company's earnings are expected to accelerate. Are these analysts expectations based on the broad expectations for the industry, or on the company's fundamentals? Click here to be taken to our analyst's forecasts page for the company.

If you’re looking to trade Tata Chemicals, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Tata Chemicals might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NSEI:TATACHEM

Tata Chemicals

Manufactures, markets, sells, and distributes basic chemistry and specialty products in India, Europe, Africa, America, rest of Asia, and internationally.

Adequate balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|22.7% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|14.2% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.8% undervalued

NO

Community Contributor