Sumitomo Chemical India Limited (NSE:SUMICHEM) Not Flying Under The Radar

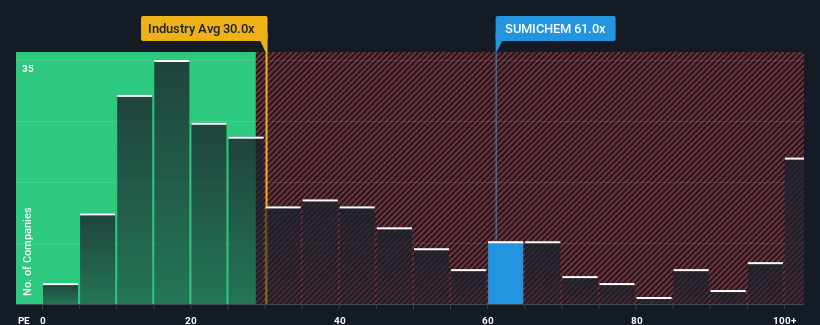

When close to half the companies in India have price-to-earnings ratios (or "P/E's") below 31x, you may consider Sumitomo Chemical India Limited (NSE:SUMICHEM) as a stock to avoid entirely with its 61x P/E ratio. However, the P/E might be quite high for a reason and it requires further investigation to determine if it's justified.

Sumitomo Chemical India could be doing better as its earnings have been going backwards lately while most other companies have been seeing positive earnings growth. One possibility is that the P/E is high because investors think this poor earnings performance will turn the corner. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

See our latest analysis for Sumitomo Chemical India

What Are Growth Metrics Telling Us About The High P/E?

The only time you'd be truly comfortable seeing a P/E as steep as Sumitomo Chemical India's is when the company's growth is on track to outshine the market decidedly.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 34%. This has soured the latest three-year period, which nevertheless managed to deliver a decent 5.6% overall rise in EPS. Accordingly, while they would have preferred to keep the run going, shareholders would be roughly satisfied with the medium-term rates of earnings growth.

Turning to the outlook, the next year should generate growth of 34% as estimated by the seven analysts watching the company. Meanwhile, the rest of the market is forecast to only expand by 24%, which is noticeably less attractive.

In light of this, it's understandable that Sumitomo Chemical India's P/E sits above the majority of other companies. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Bottom Line On Sumitomo Chemical India's P/E

Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

As we suspected, our examination of Sumitomo Chemical India's analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. It's hard to see the share price falling strongly in the near future under these circumstances.

You always need to take note of risks, for example - Sumitomo Chemical India has 1 warning sign we think you should be aware of.

Of course, you might also be able to find a better stock than Sumitomo Chemical India. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:SUMICHEM

Sumitomo Chemical India

Engages in the manufacture and sale of household and public health insecticides, agricultural pesticides, and animal nutrition products in India and internationally.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Community Narratives