Advertisement

Analysts Have Made A Financial Statement On Sumitomo Chemical India Limited's (NSE:SUMICHEM) Third-Quarter Report

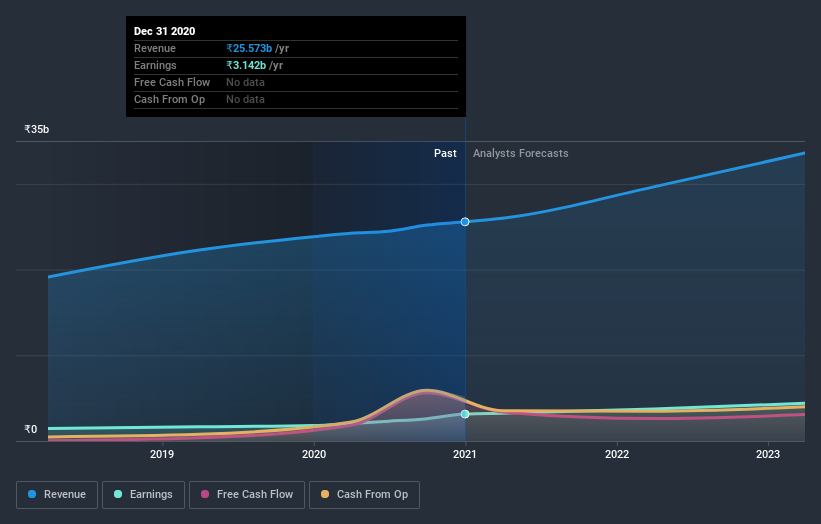

Sumitomo Chemical India Limited (NSE:SUMICHEM) shareholders are probably feeling a little disappointed, since its shares fell 2.0% to ₹308 in the week after its latest third-quarter results. Results were roughly in line with estimates, with revenues of ₹5.6b and statutory earnings per share of ₹4.10. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. So we collected the latest post-earnings statutory consensus estimates to see what could be in store for next year.

View our latest analysis for Sumitomo Chemical India

Taking into account the latest results, the current consensus from Sumitomo Chemical India's seven analysts is for revenues of ₹29.6b in 2022, which would reflect a meaningful 16% increase on its sales over the past 12 months. Statutory earnings per share are predicted to swell 17% to ₹7.35. In the lead-up to this report, the analysts had been modelling revenues of ₹30.5b and earnings per share (EPS) of ₹7.42 in 2022. So it looks like the analysts have become a bit less optimistic after the latest results announcement, with revenues expected to fall even as the company is supposed to maintain EPS.

The average price target was steady at ₹310even though revenue estimates declined; likely suggesting the analysts place a higher value on earnings. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. The most optimistic Sumitomo Chemical India analyst has a price target of ₹343 per share, while the most pessimistic values it at ₹269. This is a very narrow spread of estimates, implying either that Sumitomo Chemical India is an easy company to value, or - more likely - the analysts are relying heavily on some key assumptions.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. It's clear from the latest estimates that Sumitomo Chemical India's rate of growth is expected to accelerate meaningfully, with the forecast 16% revenue growth noticeably faster than its historical growth of 9.7%p.a. over the past three years. Compare this with other companies in the same industry, which are forecast to grow their revenue 16% next year. Factoring in the forecast acceleration in revenue, it's pretty clear that Sumitomo Chemical India is expected to grow at about the same rate as the wider industry.

The Bottom Line

The most obvious conclusion is that there's been no major change in the business' prospects in recent times, with the analysts holding their earnings forecasts steady, in line with previous estimates. They also downgraded their revenue estimates, although as we saw earlier, forecast growth is only expected to be about the same as the wider industry. With that said, earnings are more important to the long-term value of the business. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. We have estimates - from multiple Sumitomo Chemical India analysts - going out to 2023, and you can see them free on our platform here.

We also provide an overview of the Sumitomo Chemical India Board and CEO remuneration and length of tenure at the company, and whether insiders have been buying the stock, here.

When trading Sumitomo Chemical India or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NSEI:SUMICHEM

Sumitomo Chemical India

Engages in the manufacture and sale of household and public health insecticides, agricultural pesticides, and animal nutrition products in India and internationally.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|18.2% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|12.1% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.4% undervalued

NO

Community Contributor