Advertisement

- India

- /

- Metals and Mining

- /

- NSEI:ORISSAMINE

Orissa Minerals Development (NSE:ORISSAMINE) Has A Pretty Healthy Balance Sheet

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, The Orissa Minerals Development Company Limited (NSE:ORISSAMINE) does carry debt. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for Orissa Minerals Development

What Is Orissa Minerals Development's Net Debt?

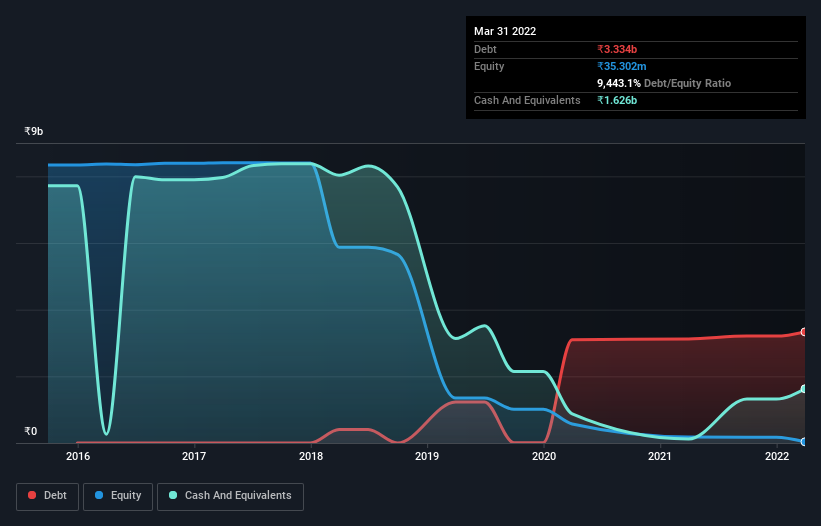

As you can see below, at the end of March 2022, Orissa Minerals Development had ₹3.33b of debt, up from ₹3.12b a year ago. Click the image for more detail. However, because it has a cash reserve of ₹1.63b, its net debt is less, at about ₹1.71b.

How Healthy Is Orissa Minerals Development's Balance Sheet?

The latest balance sheet data shows that Orissa Minerals Development had liabilities of ₹3.30b due within a year, and liabilities of ₹1.32b falling due after that. Offsetting these obligations, it had cash of ₹1.63b as well as receivables valued at ₹67.0k due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by ₹3.00b.

Since publicly traded Orissa Minerals Development shares are worth a total of ₹16.3b, it seems unlikely that this level of liabilities would be a major threat. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Weak interest cover of 0.32 times and a disturbingly high net debt to EBITDA ratio of 6.9 hit our confidence in Orissa Minerals Development like a one-two punch to the gut. The debt burden here is substantial. However, the silver lining was that Orissa Minerals Development achieved a positive EBIT of ₹95m in the last twelve months, an improvement on the prior year's loss. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Orissa Minerals Development will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So it's worth checking how much of the earnings before interest and tax (EBIT) is backed by free cash flow. Happily for any shareholders, Orissa Minerals Development actually produced more free cash flow than EBIT over the last year. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Our View

We weren't impressed with Orissa Minerals Development's net debt to EBITDA, and its interest cover made us cautious. But like a ballerina ending on a perfect pirouette, it has not trouble converting EBIT to free cash flow. Looking at all this data makes us feel a little cautious about Orissa Minerals Development's debt levels. While we appreciate debt can enhance returns on equity, we'd suggest that shareholders keep close watch on its debt levels, lest they increase. Even though Orissa Minerals Development lost money on the bottom line, its positive EBIT suggests the business itself has potential. So you might want to check out how earnings have been trending over the last few years.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:ORISSAMINE

Orissa Minerals Development

The Orissa Minerals Development Company Limited mines and markets iron ore and manganese ore in India.

Imperfect balance sheet with minimal risk.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.4% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.0% undervalued

EA

Community Contributor