Oriental Aromatics (NSE:OAL) Seems To Use Debt Rather Sparingly

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Oriental Aromatics Limited (NSE:OAL) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for Oriental Aromatics

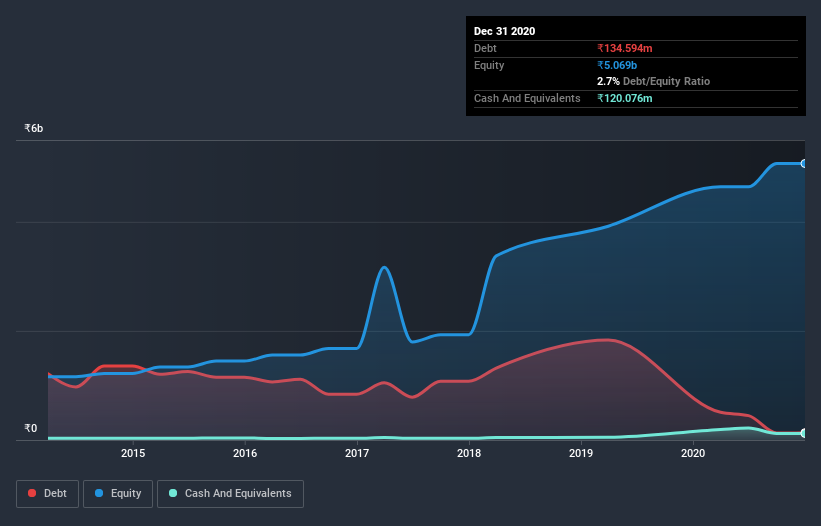

What Is Oriental Aromatics's Debt?

As you can see below, Oriental Aromatics had ₹123.5m of debt at September 2020, down from ₹507.6m a year prior. However, it also had ₹120.1m in cash, and so its net debt is ₹3.47m.

How Healthy Is Oriental Aromatics' Balance Sheet?

According to the last reported balance sheet, Oriental Aromatics had liabilities of ₹932.8m due within 12 months, and liabilities of ₹283.7m due beyond 12 months. On the other hand, it had cash of ₹120.1m and ₹1.34b worth of receivables due within a year. So it can boast ₹243.6m more liquid assets than total liabilities.

Having regard to Oriental Aromatics' size, it seems that its liquid assets are well balanced with its total liabilities. So it's very unlikely that the ₹20.4b company is short on cash, but still worth keeping an eye on the balance sheet. But either way, Oriental Aromatics has virtually no net debt, so it's fair to say it does not have a heavy debt load!

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Oriental Aromatics has very modest net debt levels, with net debt at just 0.0022 times EBITDA. Happily, it actually managed to receive more interest than it paid, over the last year. So it's fair to say it can handle debt like an Olympic ice-skater handles a pirouette. In addition to that, we're happy to report that Oriental Aromatics has boosted its EBIT by 31%, thus reducing the spectre of future debt repayments. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Oriental Aromatics will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So it's worth checking how much of that EBIT is backed by free cash flow. Over the most recent three years, Oriental Aromatics recorded free cash flow worth 60% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

Oriental Aromatics's interest cover suggests it can handle its debt as easily as Cristiano Ronaldo could score a goal against an under 14's goalkeeper. And the good news does not stop there, as its EBIT growth rate also supports that impression! Considering this range of factors, it seems to us that Oriental Aromatics is quite prudent with its debt, and the risks seem well managed. So we're not worried about the use of a little leverage on the balance sheet. Over time, share prices tend to follow earnings per share, so if you're interested in Oriental Aromatics, you may well want to click here to check an interactive graph of its earnings per share history.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

If you decide to trade Oriental Aromatics, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

If you're looking to trade Oriental Aromatics, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NSEI:OAL

Oriental Aromatics

Manufactures and sells terpene chemicals, camphor, and other specialty aroma Ingredients in India.

Excellent balance sheet with proven track record.

Market Insights

Community Narratives