Some Lead Reclaim and Rubber Products Limited (NSE:LRRPL) Shareholders Look For Exit As Shares Take 26% Pounding

Lead Reclaim and Rubber Products Limited (NSE:LRRPL) shares have retraced a considerable 26% in the last month, reversing a fair amount of their solid recent performance. To make matters worse, the recent drop has wiped out a year's worth of gains with the share price now back where it started a year ago.

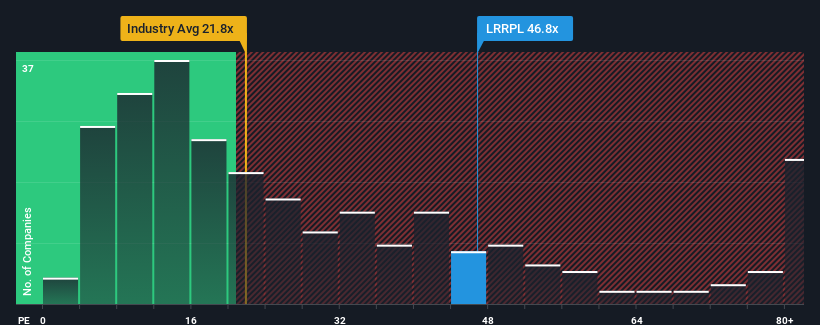

Even after such a large drop in price, Lead Reclaim and Rubber Products' price-to-earnings (or "P/E") ratio of 46.8x might still make it look like a strong sell right now compared to the market in India, where around half of the companies have P/E ratios below 25x and even P/E's below 13x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/E.

The earnings growth achieved at Lead Reclaim and Rubber Products over the last year would be more than acceptable for most companies. It might be that many expect the respectable earnings performance to beat most other companies over the coming period, which has increased investors’ willingness to pay up for the stock. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

See our latest analysis for Lead Reclaim and Rubber Products

Is There Enough Growth For Lead Reclaim and Rubber Products?

There's an inherent assumption that a company should far outperform the market for P/E ratios like Lead Reclaim and Rubber Products' to be considered reasonable.

If we review the last year of earnings growth, the company posted a worthy increase of 8.0%. Ultimately though, it couldn't turn around the poor performance of the prior period, with EPS shrinking 85% in total over the last three years. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

In contrast to the company, the rest of the market is expected to grow by 25% over the next year, which really puts the company's recent medium-term earnings decline into perspective.

With this information, we find it concerning that Lead Reclaim and Rubber Products is trading at a P/E higher than the market. Apparently many investors in the company are way more bullish than recent times would indicate and aren't willing to let go of their stock at any price. Only the boldest would assume these prices are sustainable as a continuation of recent earnings trends is likely to weigh heavily on the share price eventually.

The Final Word

Lead Reclaim and Rubber Products' shares may have retreated, but its P/E is still flying high. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

Our examination of Lead Reclaim and Rubber Products revealed its shrinking earnings over the medium-term aren't impacting its high P/E anywhere near as much as we would have predicted, given the market is set to grow. Right now we are increasingly uncomfortable with the high P/E as this earnings performance is highly unlikely to support such positive sentiment for long. If recent medium-term earnings trends continue, it will place shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

Before you settle on your opinion, we've discovered 5 warning signs for Lead Reclaim and Rubber Products (4 shouldn't be ignored!) that you should be aware of.

If you're unsure about the strength of Lead Reclaim and Rubber Products' business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:LRRPL

Lead Reclaim and Rubber Products

Manufactures and sells reclaimed rubber, crumb rubber powder, and rubber granules in India.

Proven track record slight.

Market Insights

Community Narratives