Advertisement

Indo Amines (NSE:INDOAMIN) Is Due To Pay A Dividend Of ₹0.50

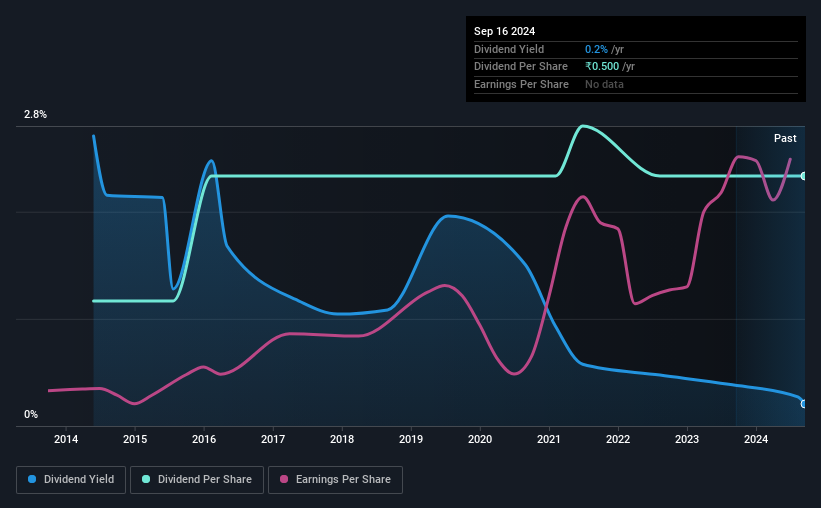

The board of Indo Amines Limited (NSE:INDOAMIN) has announced that it will pay a dividend of ₹0.50 per share on the 24th of October. This means the annual payment will be 0.2% of the current stock price, which is lower than the industry average.

While the dividend yield is important for income investors, it is also important to consider any large share price moves, as this will generally outweigh any gains from distributions. Investors will be pleased to see that Indo Amines' stock price has increased by 95% in the last 3 months, which is good for shareholders and can also explain a decrease in the dividend yield.

Check out our latest analysis for Indo Amines

Indo Amines' Future Dividend Projections Appear Well Covered By Earnings

If it is predictable over a long period, even low dividend yields can be attractive. Before making this announcement, Indo Amines was easily earning enough to cover the dividend. As a result, a large proportion of what it earned was being reinvested back into the business.

Looking forward, earnings per share could rise by 13.5% over the next year if the trend from the last few years continues. If the dividend continues on this path, the payout ratio could be 6.6% by next year, which we think can be pretty sustainable going forward.

Indo Amines Has A Solid Track Record

The company has been paying a dividend for a long time, and it has been quite stable which gives us confidence in the future dividend potential. The dividend has gone from an annual total of ₹0.25 in 2014 to the most recent total annual payment of ₹0.50. This means that it has been growing its distributions at 7.2% per annum over that time. The dividend has been growing very nicely for a number of years, and has given its shareholders some nice income in their portfolios.

The Dividend Looks Likely To Grow

Investors who have held shares in the company for the past few years will be happy with the dividend income they have received. We are encouraged to see that Indo Amines has grown earnings per share at 14% per year over the past five years. A low payout ratio and decent growth suggests that the company is reinvesting well, and it also has plenty of room to increase the dividend over time.

We Really Like Indo Amines' Dividend

Overall, we like to see the dividend staying consistent, and we think Indo Amines might even raise payments in the future. The company is easily earning enough to cover its dividend payments and it is great to see that these earnings are being translated into cash flow. All of these factors considered, we think this has solid potential as a dividend stock.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. However, there are other things to consider for investors when analysing stock performance. To that end, Indo Amines has 3 warning signs (and 1 which is a bit concerning) we think you should know about. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:INDOAMIN

Indo Amines

Engages in the manufacture, distribution, and sale of fine, performance, and specialty chemicals in India and internationally.

Outstanding track record with adequate balance sheet and pays a dividend.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|7.5% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|93.3% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|26.4% undervalued

GM

Community Contributor