- India

- /

- Metals and Mining

- /

- NSEI:IMFA

Indian Metals and Ferro Alloys Limited (NSE:IMFA) Soars 30% But It's A Story Of Risk Vs Reward

Indian Metals and Ferro Alloys Limited (NSE:IMFA) shares have continued their recent momentum with a 30% gain in the last month alone. The last month tops off a massive increase of 203% in the last year.

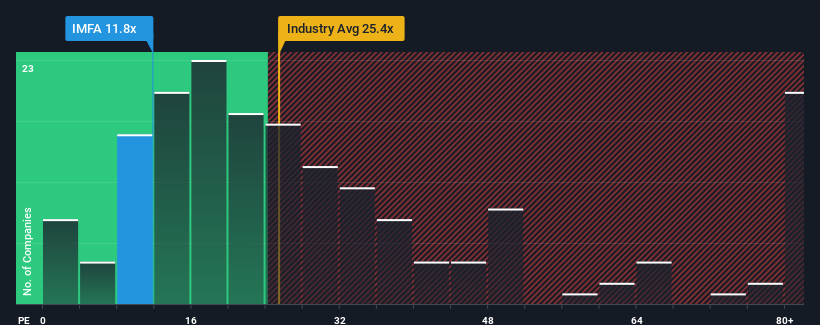

In spite of the firm bounce in price, Indian Metals and Ferro Alloys' price-to-earnings (or "P/E") ratio of 11.8x might still make it look like a strong buy right now compared to the market in India, where around half of the companies have P/E ratios above 31x and even P/E's above 61x are quite common. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so limited.

Recent times have been quite advantageous for Indian Metals and Ferro Alloys as its earnings have been rising very briskly. One possibility is that the P/E is low because investors think this strong earnings growth might actually underperform the broader market in the near future. If that doesn't eventuate, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

Check out our latest analysis for Indian Metals and Ferro Alloys

What Are Growth Metrics Telling Us About The Low P/E?

There's an inherent assumption that a company should far underperform the market for P/E ratios like Indian Metals and Ferro Alloys' to be considered reasonable.

If we review the last year of earnings growth, the company posted a terrific increase of 75%. The strong recent performance means it was also able to grow EPS by 137% in total over the last three years. So we can start by confirming that the company has done a great job of growing earnings over that time.

This is in contrast to the rest of the market, which is expected to grow by 25% over the next year, materially lower than the company's recent medium-term annualised growth rates.

In light of this, it's peculiar that Indian Metals and Ferro Alloys' P/E sits below the majority of other companies. Apparently some shareholders believe the recent performance has exceeded its limits and have been accepting significantly lower selling prices.

The Bottom Line On Indian Metals and Ferro Alloys' P/E

Shares in Indian Metals and Ferro Alloys are going to need a lot more upward momentum to get the company's P/E out of its slump. While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

We've established that Indian Metals and Ferro Alloys currently trades on a much lower than expected P/E since its recent three-year growth is higher than the wider market forecast. When we see strong earnings with faster-than-market growth, we assume potential risks are what might be placing significant pressure on the P/E ratio. At least price risks look to be very low if recent medium-term earnings trends continue, but investors seem to think future earnings could see a lot of volatility.

And what about other risks? Every company has them, and we've spotted 2 warning signs for Indian Metals and Ferro Alloys you should know about.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with a strong growth track record, trading on a low P/E.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:IMFA

Indian Metals and Ferro Alloys

Engages in the production and sale of ferro chrome in India and internationally.

Flawless balance sheet established dividend payer.

Market Insights

Community Narratives