We Wouldn't Rely On Himadri Speciality Chemical's (NSE:HSCL) Statutory Earnings As A Guide

Statistically speaking, it is less risky to invest in profitable companies than in unprofitable ones. However, sometimes companies receive a one-off boost (or reduction) to their profit, and it's not always clear whether statutory profits are a good guide, going forward. This article will consider whether Himadri Speciality Chemical's (NSE:HSCL) statutory profits are a good guide to its underlying earnings.

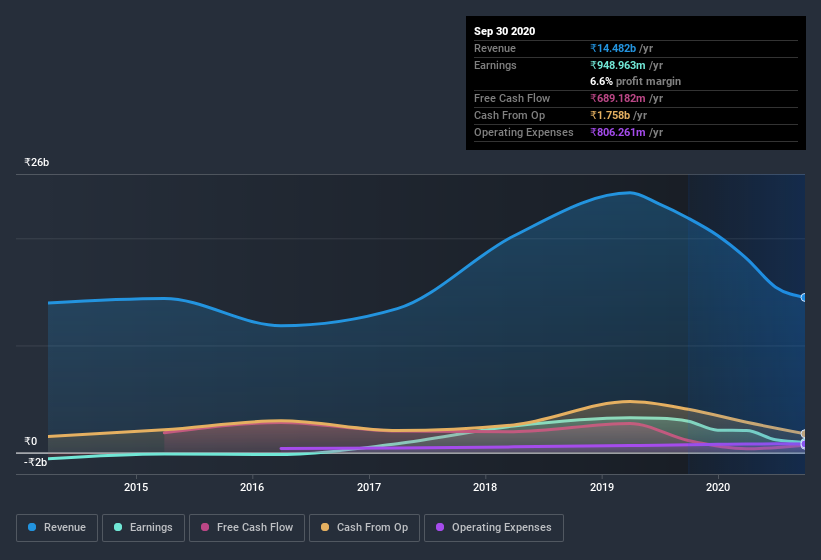

It's good to see that over the last twelve months Himadri Speciality Chemical made a profit of ₹949.0m on revenue of ₹14.5b. The chart below shows that both revenue and profit have declined over the last three years.

Check out our latest analysis for Himadri Speciality Chemical

Of course, when it comes to statutory profit, the devil is often in the detail, and we can get a better sense for a company by diving deeper into the financial statements. This article, will discuss how a tax benefit impacted Himadri Speciality Chemical's most recent profit results. That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

An Unusual Tax Situation

Himadri Speciality Chemical reported a tax benefit of ₹550m, which is well worth noting. This is of course a bit out of the ordinary, given it is more common for companies to be paying tax than receiving tax benefits! Of course, prima facie it's great to receive a tax benefit. However, our data indicates that tax benefits can temporarily boost statutory profit in the year it is booked, but subsequently profit may fall back. In the likely event the tax benefit is not repeated, we'd expect to see its statutory profit levels drop, at least in the absence of strong growth. So while we think it's great to receive a tax benefit, it does tend to imply an increased risk that the statutory profit overstates the sustainable earnings power of the business.

Our Take On Himadri Speciality Chemical's Profit Performance

As we have already discussed Himadri Speciality Chemical reported that it received a tax benefit, rather than paying tax, in the last year. Given that sort of benefit is not recurring, a focus on the statutory profit might make the company seem better than it really is. Therefore, it seems possible to us that Himadri Speciality Chemical's true underlying earnings power is actually less than its statutory profit. In further bad news, its earnings per share decreased in the last year. Of course, we've only just scratched the surface when it comes to analysing its earnings; one could also consider margins, forecast growth, and return on investment, among other factors. So while earnings quality is important, it's equally important to consider the risks facing Himadri Speciality Chemical at this point in time. At Simply Wall St, we found 3 warning signs for Himadri Speciality Chemical and we think they deserve your attention.

Today we've zoomed in on a single data point to better understand the nature of Himadri Speciality Chemical's profit. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

If you’re looking to trade Himadri Speciality Chemical, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Himadri Speciality Chemical might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NSEI:HSCL

Himadri Speciality Chemical

Manufactures and sells carbon materials and chemicals in India and internationally.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Community Narratives