Risks Still Elevated At These Prices As Hindcon Chemicals Limited (NSE:HINDCON) Shares Dive 26%

Hindcon Chemicals Limited (NSE:HINDCON) shares have had a horrible month, losing 26% after a relatively good period beforehand. Of course, over the longer-term many would still wish they owned shares as the stock's price has soared 185% in the last twelve months.

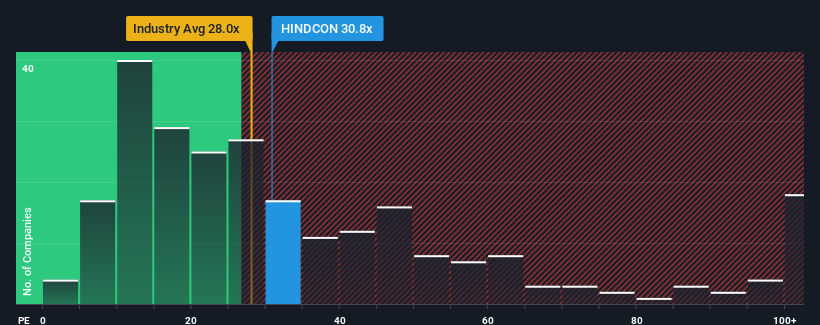

In spite of the heavy fall in price, there still wouldn't be many who think Hindcon Chemicals' price-to-earnings (or "P/E") ratio of 30.8x is worth a mention when the median P/E in India is similar at about 28x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/E.

With earnings growth that's exceedingly strong of late, Hindcon Chemicals has been doing very well. The P/E is probably moderate because investors think this strong earnings growth might not be enough to outperform the broader market in the near future. If that doesn't eventuate, then existing shareholders have reason to be feeling optimistic about the future direction of the share price.

See our latest analysis for Hindcon Chemicals

How Is Hindcon Chemicals' Growth Trending?

There's an inherent assumption that a company should be matching the market for P/E ratios like Hindcon Chemicals' to be considered reasonable.

Taking a look back first, we see that the company grew earnings per share by an impressive 37% last year. The latest three year period has also seen an excellent 32% overall rise in EPS, aided by its short-term performance. So we can start by confirming that the company has done a great job of growing earnings over that time.

This is in contrast to the rest of the market, which is expected to grow by 24% over the next year, materially higher than the company's recent medium-term annualised growth rates.

In light of this, it's curious that Hindcon Chemicals' P/E sits in line with the majority of other companies. Apparently many investors in the company are less bearish than recent times would indicate and aren't willing to let go of their stock right now. They may be setting themselves up for future disappointment if the P/E falls to levels more in line with recent growth rates.

The Key Takeaway

Following Hindcon Chemicals' share price tumble, its P/E is now hanging on to the median market P/E. Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've established that Hindcon Chemicals currently trades on a higher than expected P/E since its recent three-year growth is lower than the wider market forecast. Right now we are uncomfortable with the P/E as this earnings performance isn't likely to support a more positive sentiment for long. Unless the recent medium-term conditions improve, it's challenging to accept these prices as being reasonable.

Don't forget that there may be other risks. For instance, we've identified 3 warning signs for Hindcon Chemicals that you should be aware of.

If you're unsure about the strength of Hindcon Chemicals' business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if Hindcon Chemicals might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:HINDCON

Hindcon Chemicals

Manufactures and sells sodium silicates and construction chemicals, and related services in India and internationally.

Flawless balance sheet slight.