There Are Reasons To Feel Uneasy About Heranba Industries' (NSE:HERANBA) Returns On Capital

There are a few key trends to look for if we want to identify the next multi-bagger. Ideally, a business will show two trends; firstly a growing return on capital employed (ROCE) and secondly, an increasing amount of capital employed. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. Having said that, from a first glance at Heranba Industries (NSE:HERANBA) we aren't jumping out of our chairs at how returns are trending, but let's have a deeper look.

Return On Capital Employed (ROCE): What Is It?

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. To calculate this metric for Heranba Industries, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

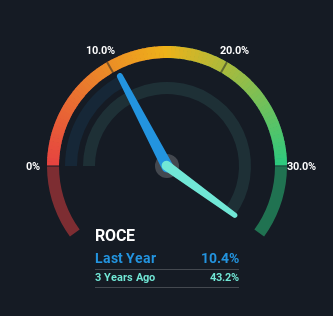

0.10 = ₹855m ÷ (₹12b - ₹3.4b) (Based on the trailing twelve months to June 2023).

Thus, Heranba Industries has an ROCE of 10%. In absolute terms, that's a pretty standard return but compared to the Chemicals industry average it falls behind.

View our latest analysis for Heranba Industries

Historical performance is a great place to start when researching a stock so above you can see the gauge for Heranba Industries' ROCE against it's prior returns. If you'd like to look at how Heranba Industries has performed in the past in other metrics, you can view this free graph of past earnings, revenue and cash flow.

What Does the ROCE Trend For Heranba Industries Tell Us?

In terms of Heranba Industries' historical ROCE movements, the trend isn't fantastic. Around five years ago the returns on capital were 56%, but since then they've fallen to 10%. Given the business is employing more capital while revenue has slipped, this is a bit concerning. If this were to continue, you might be looking at a company that is trying to reinvest for growth but is actually losing market share since sales haven't increased.

On a related note, Heranba Industries has decreased its current liabilities to 29% of total assets. That could partly explain why the ROCE has dropped. What's more, this can reduce some aspects of risk to the business because now the company's suppliers or short-term creditors are funding less of its operations. Some would claim this reduces the business' efficiency at generating ROCE since it is now funding more of the operations with its own money.

What We Can Learn From Heranba Industries' ROCE

In summary, we're somewhat concerned by Heranba Industries' diminishing returns on increasing amounts of capital. Long term shareholders who've owned the stock over the last year have experienced a 23% depreciation in their investment, so it appears the market might not like these trends either. That being the case, unless the underlying trends revert to a more positive trajectory, we'd consider looking elsewhere.

One more thing, we've spotted 2 warning signs facing Heranba Industries that you might find interesting.

While Heranba Industries isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

Valuation is complex, but we're here to simplify it.

Discover if Heranba Industries might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:HERANBA

Heranba Industries

Engages in the manufacture and sale of various agrochemicals in India.

Excellent balance sheet with acceptable track record.

Similar Companies

Market Insights

Community Narratives