Gulf Oil Lubricants India Limited's (NSE:GULFOILLUB) Shares Bounce 29% But Its Business Still Trails The Market

Gulf Oil Lubricants India Limited (NSE:GULFOILLUB) shares have had a really impressive month, gaining 29% after a shaky period beforehand. The annual gain comes to 158% following the latest surge, making investors sit up and take notice.

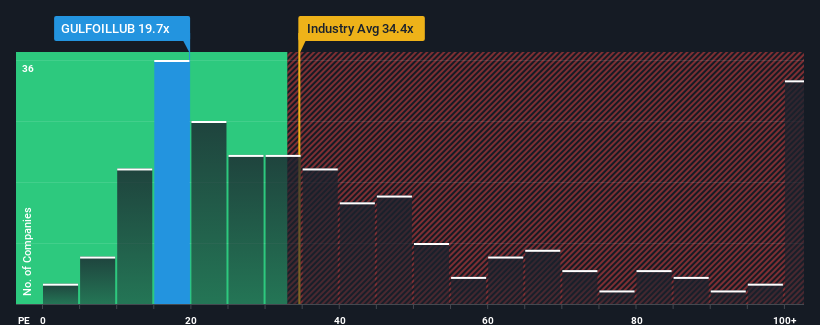

Although its price has surged higher, Gulf Oil Lubricants India may still be sending bullish signals at the moment with its price-to-earnings (or "P/E") ratio of 19.7x, since almost half of all companies in India have P/E ratios greater than 34x and even P/E's higher than 68x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/E.

Recent times have been advantageous for Gulf Oil Lubricants India as its earnings have been rising faster than most other companies. One possibility is that the P/E is low because investors think this strong earnings performance might be less impressive moving forward. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

See our latest analysis for Gulf Oil Lubricants India

Does Growth Match The Low P/E?

There's an inherent assumption that a company should underperform the market for P/E ratios like Gulf Oil Lubricants India's to be considered reasonable.

If we review the last year of earnings growth, the company posted a terrific increase of 33%. The latest three year period has also seen an excellent 57% overall rise in EPS, aided by its short-term performance. Therefore, it's fair to say the earnings growth recently has been superb for the company.

Looking ahead now, EPS is anticipated to climb by 12% each year during the coming three years according to the two analysts following the company. That's shaping up to be materially lower than the 22% per annum growth forecast for the broader market.

In light of this, it's understandable that Gulf Oil Lubricants India's P/E sits below the majority of other companies. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

The Bottom Line On Gulf Oil Lubricants India's P/E

The latest share price surge wasn't enough to lift Gulf Oil Lubricants India's P/E close to the market median. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

As we suspected, our examination of Gulf Oil Lubricants India's analyst forecasts revealed that its inferior earnings outlook is contributing to its low P/E. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. It's hard to see the share price rising strongly in the near future under these circumstances.

And what about other risks? Every company has them, and we've spotted 2 warning signs for Gulf Oil Lubricants India you should know about.

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NSEI:GULFOILLUB

Gulf Oil Lubricants India

Manufactures, markets, and trades lubricating oils, greases, and other derivatives for use in the automobile and industrial sectors in India.

Outstanding track record with flawless balance sheet and pays a dividend.

Similar Companies

Market Insights

Community Narratives