Advertisement

Commercial Syn Bags (NSE:COMSYN) Takes On Some Risk With Its Use Of Debt

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Commercial Syn Bags Limited (NSE:COMSYN) does carry debt. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for Commercial Syn Bags

What Is Commercial Syn Bags's Net Debt?

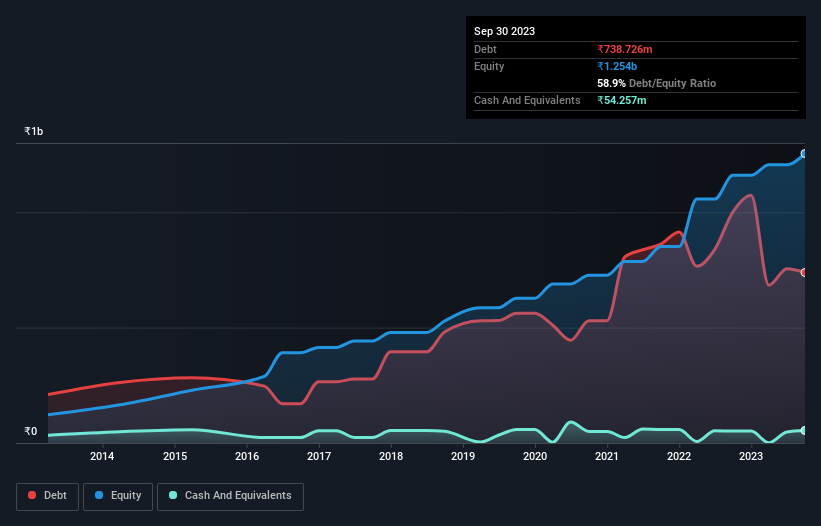

You can click the graphic below for the historical numbers, but it shows that Commercial Syn Bags had ₹738.7m of debt in September 2023, down from ₹1.00b, one year before. However, because it has a cash reserve of ₹54.3m, its net debt is less, at about ₹684.5m.

How Healthy Is Commercial Syn Bags' Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Commercial Syn Bags had liabilities of ₹684.2m due within 12 months and liabilities of ₹421.0m due beyond that. Offsetting this, it had ₹54.3m in cash and ₹331.6m in receivables that were due within 12 months. So its liabilities total ₹719.3m more than the combination of its cash and short-term receivables.

Since publicly traded Commercial Syn Bags shares are worth a total of ₹3.82b, it seems unlikely that this level of liabilities would be a major threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Commercial Syn Bags's debt is 2.5 times its EBITDA, and its EBIT cover its interest expense 3.2 times over. Taken together this implies that, while we wouldn't want to see debt levels rise, we think it can handle its current leverage. The bad news is that Commercial Syn Bags saw its EBIT decline by 18% over the last year. If earnings continue to decline at that rate then handling the debt will be more difficult than taking three children under 5 to a fancy pants restaurant. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Commercial Syn Bags will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So it's worth checking how much of that EBIT is backed by free cash flow. During the last three years, Commercial Syn Bags burned a lot of cash. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

To be frank both Commercial Syn Bags's EBIT growth rate and its track record of converting EBIT to free cash flow make us rather uncomfortable with its debt levels. Having said that, its ability to handle its total liabilities isn't such a worry. Overall, we think it's fair to say that Commercial Syn Bags has enough debt that there are some real risks around the balance sheet. If everything goes well that may pay off but the downside of this debt is a greater risk of permanent losses. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. For example Commercial Syn Bags has 3 warning signs (and 1 which is significant) we think you should know about.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:COMSYN

Commercial Syn Bags

Together with its subsidiary, Comsyn India Private Limited, engages in the manufacturing and exporting of various packaging solutions in India and internationally.

Proven track record with mediocre balance sheet.

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|44.7% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|13.0% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$646.30|7.3% undervalued

AN

Based on Analyst Price Targets