Should Bhansali Engineering Polymers Limited (NSE:BEPL) Be Part Of Your Dividend Portfolio?

Is Bhansali Engineering Polymers Limited (NSE:BEPL) a good dividend stock? How can we tell? Dividend paying companies with growing earnings can be highly rewarding in the long term. Yet sometimes, investors buy a popular dividend stock because of its yield, and then lose money if the company's dividend doesn't live up to expectations.

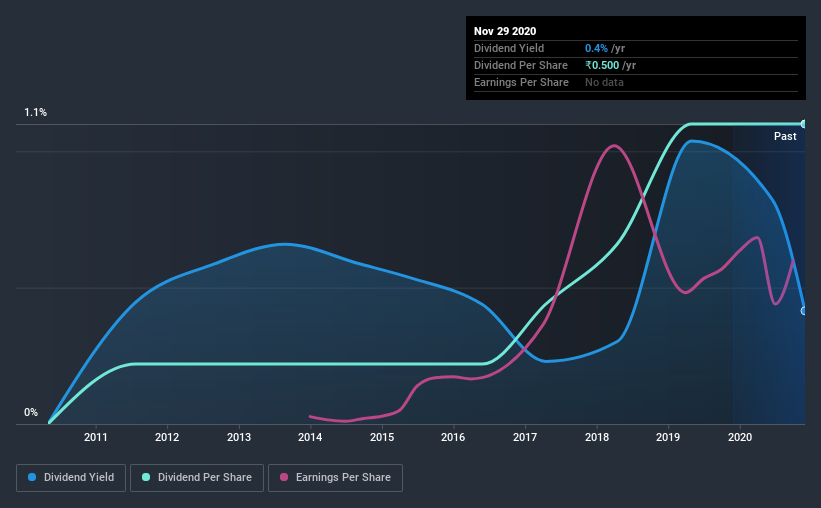

With a 0.4% yield and a nine-year payment history, investors probably think Bhansali Engineering Polymers looks like a reliable dividend stock. A low yield is generally a turn-off, but if the prospects for earnings growth were strong, investors might be pleasantly surprised by the long-term results. That said, the recent jump in the share price will make Bhansali Engineering Polymers's dividend yield look smaller, even though the company prospects could be improving. There are a few simple ways to reduce the risks of buying Bhansali Engineering Polymers for its dividend, and we'll go through these below.

Click the interactive chart for our full dividend analysis

Payout ratios

Dividends are usually paid out of company earnings. If a company is paying more than it earns, then the dividend might become unsustainable - hardly an ideal situation. So we need to form a view on if a company's dividend is sustainable, relative to its net profit after tax. In the last year, Bhansali Engineering Polymers paid out 14% of its profit as dividends. Given the low payout ratio, it is hard to envision the dividend coming under threat, barring a catastrophe.

Another important check we do is to see if the free cash flow generated is sufficient to pay the dividend. The company paid out 68% of its free cash flow, which is not bad per se, but does start to limit the amount of cash Bhansali Engineering Polymers has available to meet other needs. It's encouraging to see that the dividend is covered by both profit and cash flow. This generally suggests the dividend is sustainable, as long as earnings don't drop precipitously.

With a strong net cash balance, Bhansali Engineering Polymers investors may not have much to worry about in the near term from a dividend perspective.

Remember, you can always get a snapshot of Bhansali Engineering Polymers' latest financial position, by checking our visualisation of its financial health.

Dividend Volatility

From the perspective of an income investor who wants to earn dividends for many years, there is not much point buying a stock if its dividend is regularly cut or is not reliable. The first recorded dividend for Bhansali Engineering Polymers, in the last decade, was nine years ago. Its dividend has not fluctuated much that time, which we like, but we're conscious that the company might not yet have a track record of maintaining dividends in all economic conditions. During the past nine-year period, the first annual payment was ₹0.1 in 2011, compared to ₹0.5 last year. Dividends per share have grown at approximately 20% per year over this time.

The dividend has been growing pretty quickly, which could be enough to get us interested even though the dividend history is relatively short. Further research may be warranted.

Dividend Growth Potential

While dividend payments have been relatively reliable, it would also be nice if earnings per share (EPS) were growing, as this is essential to maintaining the dividend's purchasing power over the long term. It's good to see Bhansali Engineering Polymers has been growing its earnings per share at 65% a year over the past five years. Earnings per share have grown rapidly, and the company is retaining a majority of its earnings. We think this is ideal from an investment perspective, if the company is able to reinvest these earnings effectively.

Conclusion

Dividend investors should always want to know if a) a company's dividends are affordable, b) if there is a track record of consistent payments, and c) if the dividend is capable of growing. Firstly, we like that Bhansali Engineering Polymers pays out a low fraction of earnings. It pays out a higher percentage of its cashflow, although this is within acceptable bounds. Next, earnings growth has been good, but unfortunately the company has not been paying dividends as long as we'd like. Overall we think Bhansali Engineering Polymers is an interesting dividend stock, although it could be better.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. However, there are other things to consider for investors when analysing stock performance. For example, we've picked out 1 warning sign for Bhansali Engineering Polymers that investors should know about before committing capital to this stock.

Looking for more high-yielding dividend ideas? Try our curated list of dividend stocks with a yield above 3%.

When trading Bhansali Engineering Polymers or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Bhansali Engineering Polymers might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NSEI:BEPL

Bhansali Engineering Polymers

Operates a petrochemical company in India and internationally.

Flawless balance sheet 6 star dividend payer.