Advertisement

- India

- /

- Personal Products

- /

- NSEI:PGHH

Subdued Growth No Barrier To Procter & Gamble Hygiene and Health Care Limited's (NSE:PGHH) Price

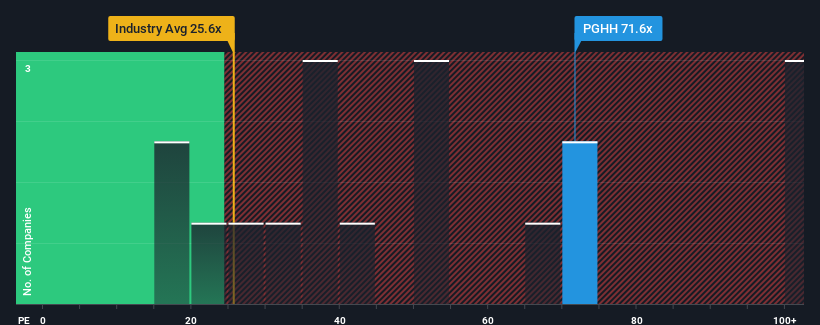

With a price-to-earnings (or "P/E") ratio of 71.6x Procter & Gamble Hygiene and Health Care Limited (NSE:PGHH) may be sending very bearish signals at the moment, given that almost half of all companies in India have P/E ratios under 32x and even P/E's lower than 18x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so lofty.

Procter & Gamble Hygiene and Health Care could be doing better as its earnings have been going backwards lately while most other companies have been seeing positive earnings growth. One possibility is that the P/E is high because investors think this poor earnings performance will turn the corner. If not, then existing shareholders may be extremely nervous about the viability of the share price.

Check out our latest analysis for Procter & Gamble Hygiene and Health Care

Is There Enough Growth For Procter & Gamble Hygiene and Health Care?

There's an inherent assumption that a company should far outperform the market for P/E ratios like Procter & Gamble Hygiene and Health Care's to be considered reasonable.

Retrospectively, the last year delivered a frustrating 7.9% decrease to the company's bottom line. That put a dampener on the good run it was having over the longer-term as its three-year EPS growth is still a noteworthy 9.7% in total. So we can start by confirming that the company has generally done a good job of growing earnings over that time, even though it had some hiccups along the way.

Shifting to the future, estimates from the two analysts covering the company suggest earnings should grow by 15% per annum over the next three years. Meanwhile, the rest of the market is forecast to expand by 19% per annum, which is noticeably more attractive.

In light of this, it's alarming that Procter & Gamble Hygiene and Health Care's P/E sits above the majority of other companies. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. There's a good chance these shareholders are setting themselves up for future disappointment if the P/E falls to levels more in line with the growth outlook.

The Bottom Line On Procter & Gamble Hygiene and Health Care's P/E

It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've established that Procter & Gamble Hygiene and Health Care currently trades on a much higher than expected P/E since its forecast growth is lower than the wider market. When we see a weak earnings outlook with slower than market growth, we suspect the share price is at risk of declining, sending the high P/E lower. Unless these conditions improve markedly, it's very challenging to accept these prices as being reasonable.

Before you take the next step, you should know about the 1 warning sign for Procter & Gamble Hygiene and Health Care that we have uncovered.

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:PGHH

Procter & Gamble Hygiene and Health Care

Manufactures and sells branded packaged fast-moving consumer goods in the feminine care and healthcare businesses in India and internationally.

Flawless balance sheet with acceptable track record.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.4% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|92.1% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|24.2% undervalued

GM

Community Contributor