- India

- /

- Personal Products

- /

- NSEI:PGHH

Procter & Gamble Hygiene and Health Care Limited's (NSE:PGHH) Business Is Trailing The Market But Its Shares Aren't

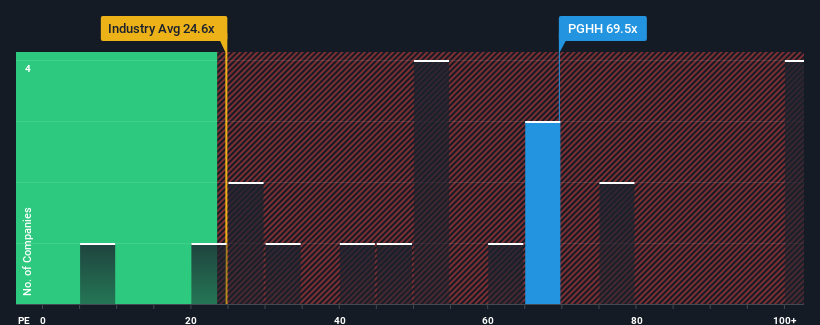

Procter & Gamble Hygiene and Health Care Limited's (NSE:PGHH) price-to-earnings (or "P/E") ratio of 69.5x might make it look like a strong sell right now compared to the market in India, where around half of the companies have P/E ratios below 31x and even P/E's below 17x are quite common. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so lofty.

Recent times have been advantageous for Procter & Gamble Hygiene and Health Care as its earnings have been rising faster than most other companies. The P/E is probably high because investors think this strong earnings performance will continue. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

See our latest analysis for Procter & Gamble Hygiene and Health Care

Is There Enough Growth For Procter & Gamble Hygiene and Health Care?

There's an inherent assumption that a company should far outperform the market for P/E ratios like Procter & Gamble Hygiene and Health Care's to be considered reasonable.

Taking a look back first, we see that the company grew earnings per share by an impressive 49% last year. The latest three year period has also seen a 14% overall rise in EPS, aided extensively by its short-term performance. Therefore, it's fair to say the earnings growth recently has been respectable for the company.

Looking ahead now, EPS is anticipated to climb by 9.9% per year during the coming three years according to the two analysts following the company. With the market predicted to deliver 20% growth each year, the company is positioned for a weaker earnings result.

With this information, we find it concerning that Procter & Gamble Hygiene and Health Care is trading at a P/E higher than the market. Apparently many investors in the company are way more bullish than analysts indicate and aren't willing to let go of their stock at any price. Only the boldest would assume these prices are sustainable as this level of earnings growth is likely to weigh heavily on the share price eventually.

What We Can Learn From Procter & Gamble Hygiene and Health Care's P/E?

It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've established that Procter & Gamble Hygiene and Health Care currently trades on a much higher than expected P/E since its forecast growth is lower than the wider market. Right now we are increasingly uncomfortable with the high P/E as the predicted future earnings aren't likely to support such positive sentiment for long. This places shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

It is also worth noting that we have found 1 warning sign for Procter & Gamble Hygiene and Health Care that you need to take into consideration.

It's important to make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:PGHH

Procter & Gamble Hygiene and Health Care

Engages in the manufacture and sale of branded packaged fast-moving consumer goods in the feminine care and healthcare businesses in India and internationally.

Excellent balance sheet with acceptable track record.

Market Insights

Community Narratives