- India

- /

- Healthcare Services

- /

- NSEI:NH

Narayana Hrudayalaya Limited (NSE:NH) Investors Are Less Pessimistic Than Expected

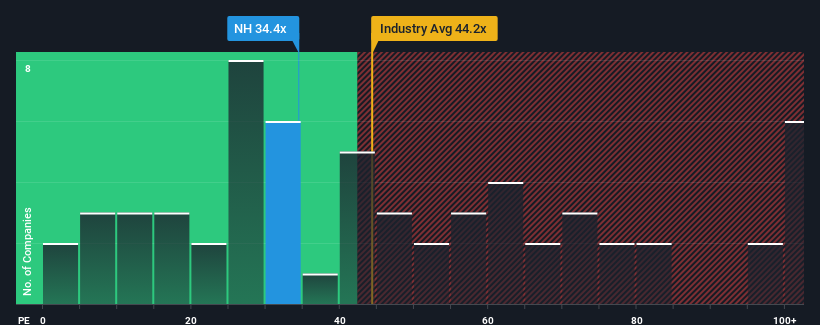

There wouldn't be many who think Narayana Hrudayalaya Limited's (NSE:NH) price-to-earnings (or "P/E") ratio of 34.4x is worth a mention when the median P/E in India is similar at about 32x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/E.

Recent times haven't been advantageous for Narayana Hrudayalaya as its earnings have been rising slower than most other companies. It might be that many expect the uninspiring earnings performance to strengthen positively, which has kept the P/E from falling. You'd really hope so, otherwise you're paying a relatively elevated price for a company with this sort of growth profile.

View our latest analysis for Narayana Hrudayalaya

Does Growth Match The P/E?

The only time you'd be comfortable seeing a P/E like Narayana Hrudayalaya's is when the company's growth is tracking the market closely.

Retrospectively, the last year delivered a decent 5.6% gain to the company's bottom line. Pleasingly, EPS has also lifted 174% in aggregate from three years ago, partly thanks to the last 12 months of growth. Therefore, it's fair to say the earnings growth recently has been superb for the company.

Turning to the outlook, the next three years should generate growth of 11% per year as estimated by the analysts watching the company. With the market predicted to deliver 19% growth per annum, the company is positioned for a weaker earnings result.

In light of this, it's curious that Narayana Hrudayalaya's P/E sits in line with the majority of other companies. It seems most investors are ignoring the fairly limited growth expectations and are willing to pay up for exposure to the stock. Maintaining these prices will be difficult to achieve as this level of earnings growth is likely to weigh down the shares eventually.

The Final Word

While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

Our examination of Narayana Hrudayalaya's analyst forecasts revealed that its inferior earnings outlook isn't impacting its P/E as much as we would have predicted. Right now we are uncomfortable with the P/E as the predicted future earnings aren't likely to support a more positive sentiment for long. This places shareholders' investments at risk and potential investors in danger of paying an unnecessary premium.

We don't want to rain on the parade too much, but we did also find 2 warning signs for Narayana Hrudayalaya (1 makes us a bit uncomfortable!) that you need to be mindful of.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with a strong growth track record, trading on a low P/E.

Valuation is complex, but we're here to simplify it.

Discover if Narayana Hrudayalaya might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:NH

Narayana Hrudayalaya

Engages in the medical and healthcare services in India and internationally.

Flawless balance sheet and fair value.