Advertisement

- India

- /

- Oil and Gas

- /

- NSEI:OIL

Oil India Limited (NSE:OIL) Stock Rockets 25% But Many Are Still Ignoring The Company

Oil India Limited (NSE:OIL) shares have continued their recent momentum with a 25% gain in the last month alone. The last month tops off a massive increase of 232% in the last year.

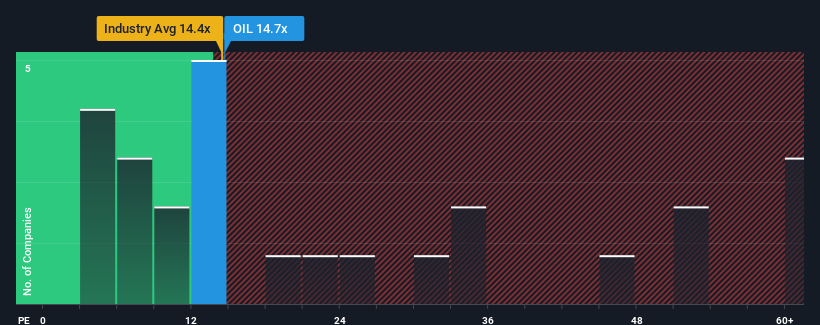

Even after such a large jump in price, Oil India may still be sending very bullish signals at the moment with its price-to-earnings (or "P/E") ratio of 14.7x, since almost half of all companies in India have P/E ratios greater than 34x and even P/E's higher than 66x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so limited.

Oil India hasn't been tracking well recently as its declining earnings compare poorly to other companies, which have seen some growth on average. It seems that many are expecting the dour earnings performance to persist, which has repressed the P/E. If you still like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

See our latest analysis for Oil India

Is There Any Growth For Oil India?

In order to justify its P/E ratio, Oil India would need to produce anemic growth that's substantially trailing the market.

Retrospectively, the last year delivered a frustrating 27% decrease to the company's bottom line. Even so, admirably EPS has lifted 80% in aggregate from three years ago, notwithstanding the last 12 months. So we can start by confirming that the company has generally done a very good job of growing earnings over that time, even though it had some hiccups along the way.

Looking ahead now, EPS is anticipated to climb by 21% each year during the coming three years according to the eleven analysts following the company. With the market predicted to deliver 22% growth per year, the company is positioned for a comparable earnings result.

With this information, we find it odd that Oil India is trading at a P/E lower than the market. Apparently some shareholders are doubtful of the forecasts and have been accepting lower selling prices.

The Bottom Line On Oil India's P/E

Shares in Oil India are going to need a lot more upward momentum to get the company's P/E out of its slump. While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

Our examination of Oil India's analyst forecasts revealed that its market-matching earnings outlook isn't contributing to its P/E as much as we would have predicted. When we see an average earnings outlook with market-like growth, we assume potential risks are what might be placing pressure on the P/E ratio. It appears some are indeed anticipating earnings instability, because these conditions should normally provide more support to the share price.

And what about other risks? Every company has them, and we've spotted 2 warning signs for Oil India you should know about.

You might be able to find a better investment than Oil India. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NSEI:OIL

Oil India

Engages in the exploration, development, and production of crude oil and natural gas in India.

Undervalued with solid track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.6% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|48.2% undervalued

TO

Community Contributor