- India

- /

- Capital Markets

- /

- NSEI:MOTILALOFS

We Ran A Stock Scan For Earnings Growth And Motilal Oswal Financial Services (NSE:MOTILALOFS) Passed With Ease

For beginners, it can seem like a good idea (and an exciting prospect) to buy a company that tells a good story to investors, even if it currently lacks a track record of revenue and profit. But as Peter Lynch said in One Up On Wall Street, 'Long shots almost never pay off.' Loss-making companies are always racing against time to reach financial sustainability, so investors in these companies may be taking on more risk than they should.

If this kind of company isn't your style, you like companies that generate revenue, and even earn profits, then you may well be interested in Motilal Oswal Financial Services (NSE:MOTILALOFS). Now this is not to say that the company presents the best investment opportunity around, but profitability is a key component to success in business.

Check out our latest analysis for Motilal Oswal Financial Services

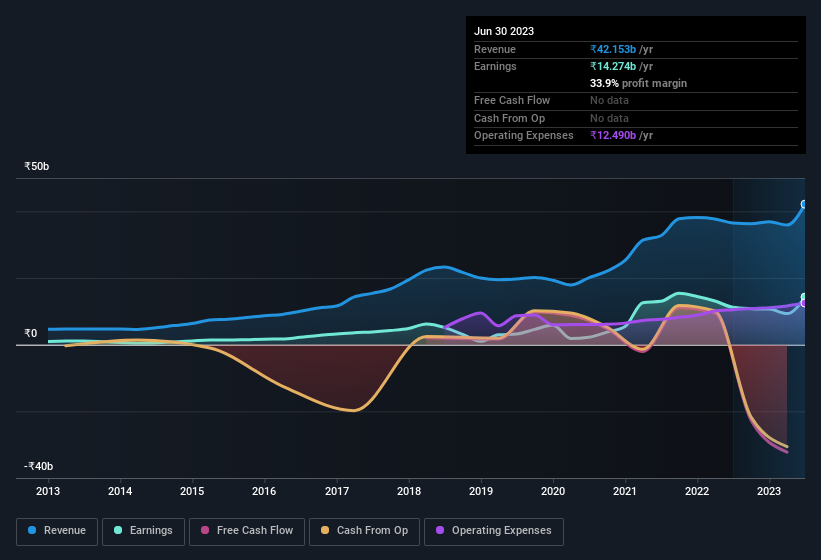

Motilal Oswal Financial Services' Improving Profits

In the last three years Motilal Oswal Financial Services' earnings per share took off; so much so that it's a bit disingenuous to use these figures to try and deduce long term estimates. So it would be better to isolate the growth rate over the last year for our analysis. Motilal Oswal Financial Services' EPS shot up from ₹76.18 to ₹96.29; a result that's bound to keep shareholders happy. That's a commendable gain of 26%.

Careful consideration of revenue growth and earnings before interest and taxation (EBIT) margins can help inform a view on the sustainability of the recent profit growth. Not all of Motilal Oswal Financial Services' revenue this year is revenue from operations, so keep in mind the revenue and margin numbers used in this article might not be the best representation of the underlying business. EBIT margins for Motilal Oswal Financial Services remained fairly unchanged over the last year, however the company should be pleased to report its revenue growth for the period of 15% to ₹42b. That's a real positive.

You can take a look at the company's revenue and earnings growth trend, in the chart below. Click on the chart to see the exact numbers.

Of course the knack is to find stocks that have their best days in the future, not in the past. You could base your opinion on past performance, of course, but you may also want to check this interactive graph of professional analyst EPS forecasts for Motilal Oswal Financial Services.

Are Motilal Oswal Financial Services Insiders Aligned With All Shareholders?

Insider interest in a company always sparks a bit of intrigue and many investors are on the lookout for companies where insiders are putting their money where their mouth is. That's because insider buying often indicates that those closest to the company have confidence that the share price will perform well. However, insiders are sometimes wrong, and we don't know the exact thinking behind their acquisitions.

We do note that, in the last year, insiders sold ₹68m worth of shares. But that's far less than the ₹205m insiders spent purchasing stock. This adds to the interest in Motilal Oswal Financial Services because it suggests that those who understand the company best, are optimistic. It is also worth noting that it was Co-Founder Motilal Oswal who made the biggest single purchase, worth ₹73m, paying ₹562 per share.

And the insider buying isn't the only sign of alignment between shareholders and the board, since Motilal Oswal Financial Services insiders own more than a third of the company. In fact, they own 76% of the company, so they will share in the same delights and challenges experienced by the ordinary shareholders. This should be seen as a good thing, as it means insiders have a personal interest in delivering the best outcomes for shareholders. ₹105b That means they have plenty of their own capital riding on the performance of the business!

While insiders already own a significant amount of shares, and they have been buying more, the good news for ordinary shareholders does not stop there. The cherry on top is that the CEO, Motilal Oswal is paid comparatively modestly to CEOs at similar sized companies. The median total compensation for CEOs of companies similar in size to Motilal Oswal Financial Services, with market caps between ₹83b and ₹266b, is around ₹41m.

The Motilal Oswal Financial Services CEO received ₹24m in compensation for the year ending March 2023. That is actually below the median for CEO's of similarly sized companies. CEO remuneration levels are not the most important metric for investors, but when the pay is modest, that does support enhanced alignment between the CEO and the ordinary shareholders. Generally, arguments can be made that reasonable pay levels attest to good decision-making.

Does Motilal Oswal Financial Services Deserve A Spot On Your Watchlist?

You can't deny that Motilal Oswal Financial Services has grown its earnings per share at a very impressive rate. That's attractive. Furthermore, company insiders have been adding to their significant stake in the company. Astute investors will want to keep this stock on watch. Don't forget that there may still be risks. For instance, we've identified 3 warning signs for Motilal Oswal Financial Services (2 are concerning) you should be aware of.

Keen growth investors love to see insider buying. Thankfully, Motilal Oswal Financial Services isn't the only one. You can see a a free list of them here.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:MOTILALOFS

Solid track record, good value and pays a dividend.

Similar Companies

Market Insights

Community Narratives