- India

- /

- Capital Markets

- /

- NSEI:INDBANK

Indbank Merchant Banking Services Limited (NSE:INDBANK) Soars 28% But It's A Story Of Risk Vs Reward

Indbank Merchant Banking Services Limited (NSE:INDBANK) shareholders have had their patience rewarded with a 28% share price jump in the last month. Looking back a bit further, it's encouraging to see the stock is up 46% in the last year.

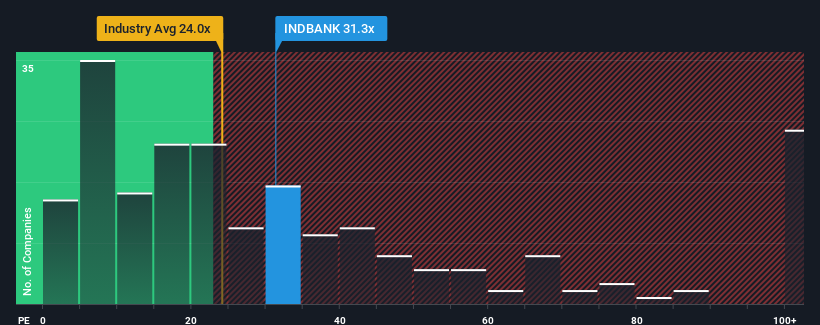

Although its price has surged higher, it's still not a stretch to say that Indbank Merchant Banking Services' price-to-earnings (or "P/E") ratio of 31.3x right now seems quite "middle-of-the-road" compared to the market in India, where the median P/E ratio is around 31x. While this might not raise any eyebrows, if the P/E ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

Indbank Merchant Banking Services has been doing a good job lately as it's been growing earnings at a solid pace. One possibility is that the P/E is moderate because investors think this respectable earnings growth might not be enough to outperform the broader market in the near future. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's not quite in favour.

See our latest analysis for Indbank Merchant Banking Services

Does Growth Match The P/E?

There's an inherent assumption that a company should be matching the market for P/E ratios like Indbank Merchant Banking Services' to be considered reasonable.

Retrospectively, the last year delivered an exceptional 17% gain to the company's bottom line. The latest three year period has also seen an excellent 119% overall rise in EPS, aided by its short-term performance. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

This is in contrast to the rest of the market, which is expected to grow by 25% over the next year, materially lower than the company's recent medium-term annualised growth rates.

In light of this, it's curious that Indbank Merchant Banking Services' P/E sits in line with the majority of other companies. Apparently some shareholders believe the recent performance is at its limits and have been accepting lower selling prices.

What We Can Learn From Indbank Merchant Banking Services' P/E?

Indbank Merchant Banking Services' stock has a lot of momentum behind it lately, which has brought its P/E level with the market. Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've established that Indbank Merchant Banking Services currently trades on a lower than expected P/E since its recent three-year growth is higher than the wider market forecast. There could be some unobserved threats to earnings preventing the P/E ratio from matching this positive performance. At least the risk of a price drop looks to be subdued if recent medium-term earnings trends continue, but investors seem to think future earnings could see some volatility.

Before you take the next step, you should know about the 2 warning signs for Indbank Merchant Banking Services that we have uncovered.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with a strong growth track record, trading on a low P/E.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:INDBANK

Indbank Merchant Banking Services

Engages in the provision of merchant banking, stock broking, depository participant, and allied services in India.

Flawless balance sheet with acceptable track record.

Market Insights

Community Narratives