- India

- /

- Hospitality

- /

- NSEI:THOMASCOOK

Thomas Cook (India) Limited's (NSE:THOMASCOOK) Share Price Boosted 32% But Its Business Prospects Need A Lift Too

Despite an already strong run, Thomas Cook (India) Limited (NSE:THOMASCOOK) shares have been powering on, with a gain of 32% in the last thirty days. The annual gain comes to 222% following the latest surge, making investors sit up and take notice.

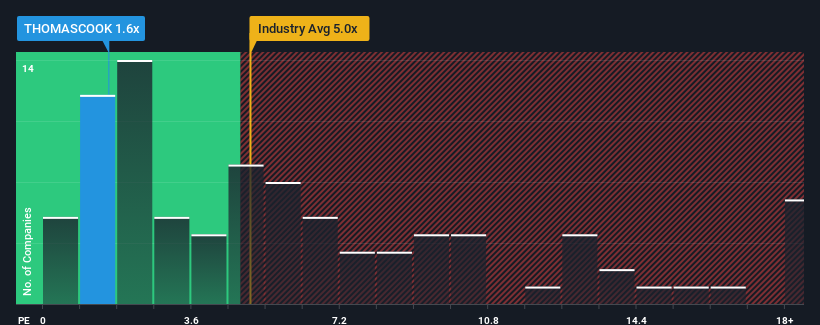

Although its price has surged higher, Thomas Cook (India) may still be sending very bullish signals at the moment with its price-to-sales (or "P/S") ratio of 1.6x, since almost half of all companies in the Hospitality industry in India have P/S ratios greater than 5x and even P/S higher than 9x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly reduced P/S.

See our latest analysis for Thomas Cook (India)

How Thomas Cook (India) Has Been Performing

Thomas Cook (India) certainly has been doing a good job lately as it's been growing revenue more than most other companies. One possibility is that the P/S ratio is low because investors think this strong revenue performance might be less impressive moving forward. If not, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

Want the full picture on analyst estimates for the company? Then our free report on Thomas Cook (India) will help you uncover what's on the horizon.How Is Thomas Cook (India)'s Revenue Growth Trending?

There's an inherent assumption that a company should far underperform the industry for P/S ratios like Thomas Cook (India)'s to be considered reasonable.

If we review the last year of revenue growth, the company posted a terrific increase of 45%. Spectacularly, three year revenue growth has ballooned by several orders of magnitude, thanks in part to the last 12 months of revenue growth. Accordingly, shareholders would have been over the moon with those medium-term rates of revenue growth.

Looking ahead now, revenue is anticipated to climb by 20% during the coming year according to the two analysts following the company. Meanwhile, the rest of the industry is forecast to expand by 30%, which is noticeably more attractive.

In light of this, it's understandable that Thomas Cook (India)'s P/S sits below the majority of other companies. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

The Key Takeaway

Even after such a strong price move, Thomas Cook (India)'s P/S still trails the rest of the industry. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

We've established that Thomas Cook (India) maintains its low P/S on the weakness of its forecast growth being lower than the wider industry, as expected. Shareholders' pessimism on the revenue prospects for the company seems to be the main contributor to the depressed P/S. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

You should always think about risks. Case in point, we've spotted 1 warning sign for Thomas Cook (India) you should be aware of.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're here to simplify it.

Discover if Thomas Cook (India) might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NSEI:THOMASCOOK

Thomas Cook (India)

Offers integrated travel services in India and internationally.

Undervalued with reasonable growth potential.

Similar Companies

Market Insights

Community Narratives