The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Country Club Hospitality & Holidays Limited (NSE:CCHHL) makes use of debt. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for Country Club Hospitality & Holidays

What Is Country Club Hospitality & Holidays's Net Debt?

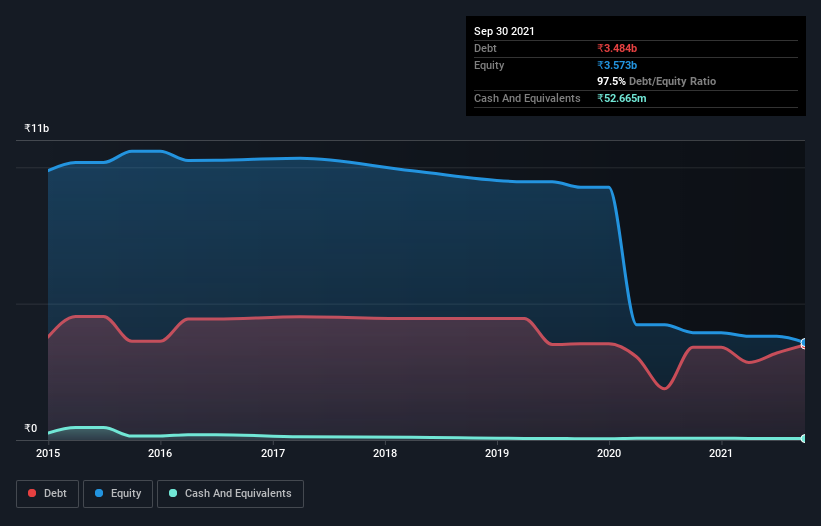

As you can see below, Country Club Hospitality & Holidays had ₹3.48b of debt, at September 2021, which is about the same as the year before. You can click the chart for greater detail. And it doesn't have much cash, so its net debt is about the same.

A Look At Country Club Hospitality & Holidays' Liabilities

According to the last reported balance sheet, Country Club Hospitality & Holidays had liabilities of ₹2.41b due within 12 months, and liabilities of ₹2.77b due beyond 12 months. On the other hand, it had cash of ₹52.7m and ₹632.2m worth of receivables due within a year. So it has liabilities totalling ₹4.49b more than its cash and near-term receivables, combined.

This deficit casts a shadow over the ₹1.24b company, like a colossus towering over mere mortals. So we definitely think shareholders need to watch this one closely. At the end of the day, Country Club Hospitality & Holidays would probably need a major re-capitalization if its creditors were to demand repayment. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Country Club Hospitality & Holidays will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year Country Club Hospitality & Holidays had a loss before interest and tax, and actually shrunk its revenue by 23%, to ₹625m. To be frank that doesn't bode well.

Caveat Emptor

Not only did Country Club Hospitality & Holidays's revenue slip over the last twelve months, but it also produced negative earnings before interest and tax (EBIT). Indeed, it lost a very considerable ₹164m at the EBIT level. If you consider the significant liabilities mentioned above, we are extremely wary of this investment. That said, it is possible that the company will turn its fortunes around. But we think that is unlikely since it is low on liquid assets, and made a loss of ₹385m in the last year. So we think this stock is quite risky. We'd prefer to pass. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. Case in point: We've spotted 2 warning signs for Country Club Hospitality & Holidays you should be aware of, and 1 of them can't be ignored.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:CCHHL

Country Club Hospitality & Holidays

Provides leisure hospitality membership services in India and the Middle East.

Low and slightly overvalued.