Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Whirlpool of India Limited (NSE:WHIRLPOOL) does use debt in its business. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for Whirlpool of India

What Is Whirlpool of India's Debt?

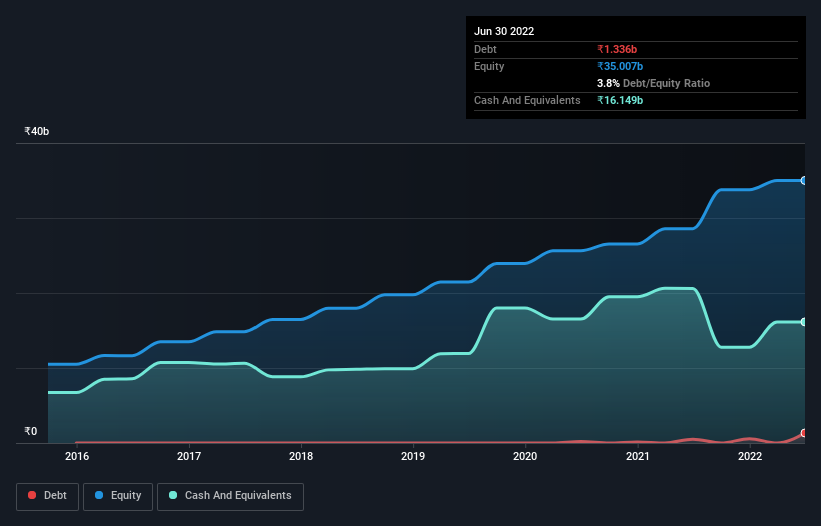

As you can see below, at the end of March 2022, Whirlpool of India had ₹1.34b of debt, up from ₹508.3m a year ago. Click the image for more detail. However, its balance sheet shows it holds ₹16.1b in cash, so it actually has ₹14.8b net cash.

How Healthy Is Whirlpool of India's Balance Sheet?

We can see from the most recent balance sheet that Whirlpool of India had liabilities of ₹17.6b falling due within a year, and liabilities of ₹4.30b due beyond that. On the other hand, it had cash of ₹16.1b and ₹4.89b worth of receivables due within a year. So its liabilities total ₹820.9m more than the combination of its cash and short-term receivables.

This state of affairs indicates that Whirlpool of India's balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So while it's hard to imagine that the ₹233.1b company is struggling for cash, we still think it's worth monitoring its balance sheet. Despite its noteworthy liabilities, Whirlpool of India boasts net cash, so it's fair to say it does not have a heavy debt load!

But the bad news is that Whirlpool of India has seen its EBIT plunge 16% in the last twelve months. If that rate of decline in earnings continues, the company could find itself in a tight spot. There's no doubt that we learn most about debt from the balance sheet. But it is Whirlpool of India's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. While Whirlpool of India has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. In the last three years, Whirlpool of India created free cash flow amounting to 8.8% of its EBIT, an uninspiring performance. That limp level of cash conversion undermines its ability to manage and pay down debt.

Summing Up

We could understand if investors are concerned about Whirlpool of India's liabilities, but we can be reassured by the fact it has has net cash of ₹14.8b. So we are not troubled with Whirlpool of India's debt use. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. Be aware that Whirlpool of India is showing 1 warning sign in our investment analysis , you should know about...

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Valuation is complex, but we're here to simplify it.

Discover if Whirlpool of India might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:WHIRLPOOL

Whirlpool of India

Manufactures and markets home appliances in India and internationally.

Excellent balance sheet with reasonable growth potential.

Market Insights

Community Narratives