Should You Be Adding Salona Cotspin (NSE:SALONA) To Your Watchlist Today?

For beginners, it can seem like a good idea (and an exciting prospect) to buy a company that tells a good story to investors, even if it completely lacks a track record of revenue and profit. Unfortunately, high risk investments often have little probability of ever paying off, and many investors pay a price to learn their lesson.

So if you're like me, you might be more interested in profitable, growing companies, like Salona Cotspin (NSE:SALONA). Now, I'm not saying that the stock is necessarily undervalued today; but I can't shake an appreciation for the profitability of the business itself. In comparison, loss making companies act like a sponge for capital - but unlike such a sponge they do not always produce something when squeezed.

View our latest analysis for Salona Cotspin

Salona Cotspin's Earnings Per Share Are Growing.

If you believe that markets are even vaguely efficient, then over the long term you'd expect a company's share price to follow its earnings per share (EPS). That makes EPS growth an attractive quality for any company. Who among us would not applaud Salona Cotspin's stratospheric annual EPS growth of 43%, compound, over the last three years? Growth that fast may well be fleeting, but like a lotus blooming from a murky pond, it sparks joy for the wary stock pickers.

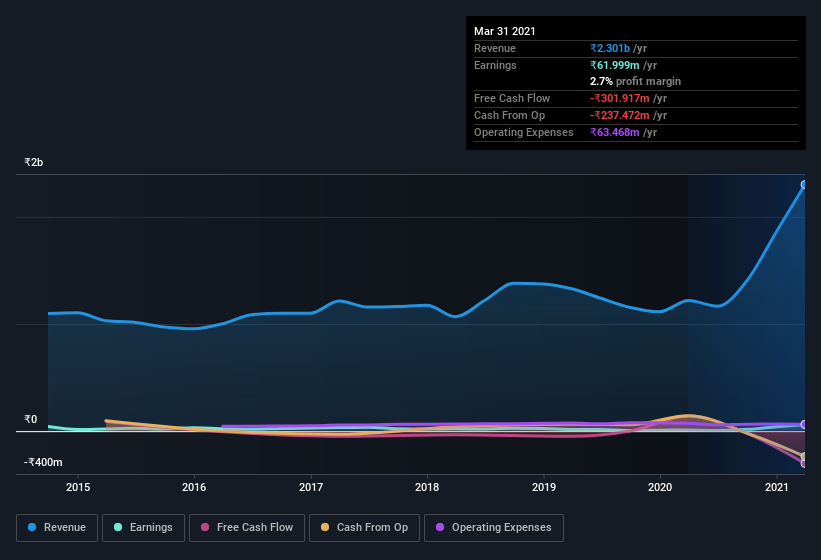

I like to see top-line growth as an indication that growth is sustainable, and I look for a high earnings before interest and taxation (EBIT) margin to point to a competitive moat (though some companies with low margins also have moats). Salona Cotspin maintained stable EBIT margins over the last year, all while growing revenue 89% to ₹2.3b. That's progress.

The chart below shows how the company's bottom and top lines have progressed over time. Click on the chart to see the exact numbers.

Since Salona Cotspin is no giant, with a market capitalization of ₹1.2b, so you should definitely check its cash and debt before getting too excited about its prospects.

Are Salona Cotspin Insiders Aligned With All Shareholders?

Like standing at the lookout, surveying the horizon at sunrise, insider buying, for some investors, sparks joy. Because oftentimes, the purchase of stock is a sign that the buyer views it as undervalued. However, insiders are sometimes wrong, and we don't know the exact thinking behind their acquisitions.

Not only did Salona Cotspin insiders refrain from selling stock during the year, but they also spent ₹12m buying it. That's nice to see, because it suggests insiders are optimistic. We also note that it was the Chairman, Shyamlal Agarwala, who made the biggest single acquisition, paying ₹1.9m for shares at about ₹58.00 each.

And the insider buying isn't the only sign of alignment between shareholders and the board, since Salona Cotspin insiders own more than a third of the company. In fact, they own 74% of the company, so they will share in the same delights and challenges experienced by the ordinary shareholders. To me this is a good sign because it suggests they will be incentivised to build value for shareholders over the long term. Of course, Salona Cotspin is a very small company, with a market cap of only ₹1.2b. That means insiders only have ₹894m worth of shares, despite the large proportional holding. That's not a huge stake in absolute terms, but it should help keep insiders aligned with other shareholders.

While insiders already own a significant amount of shares, and they have been buying more, the good news for ordinary shareholders does not stop there. That's because on our analysis the CEO, Shyamlal Agarwala, is paid less than the median for similar sized companies. I discovered that the median total compensation for the CEOs of companies like Salona Cotspin with market caps under ₹15b is about ₹2.9m.

The Salona Cotspin CEO received total compensation of only ₹2.6m in the year to . This could be considered a token amount, and indicates that the company does not need to use payment to motivate the CEO - that is often a good sign. CEO remuneration levels are not the most important metric for investors, but when the pay is modest, that does support enhanced alignment between the CEO and the ordinary shareholders. I'd also argue reasonable pay levels attest to good decision making more generally.

Is Salona Cotspin Worth Keeping An Eye On?

Salona Cotspin's earnings per share have taken off like a rocket aimed right at the moon. What's more insiders own a significant stake in the company and have been buying more shares. Because of the potential that it has reached an inflection point, I'd suggest Salona Cotspin belongs on the top of your watchlist. You should always think about risks though. Case in point, we've spotted 5 warning signs for Salona Cotspin you should be aware of, and 2 of them don't sit too well with us.

There are plenty of other companies that have insiders buying up shares. So if you like the sound of Salona Cotspin, you'll probably love this free list of growing companies that insiders are buying.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

If you’re looking to trade Salona Cotspin, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

If you're looking to trade Salona Cotspin, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NSEI:SALONA

Salona Cotspin

Produces and sells cotton yarn, knitted fabrics, and garments in India.

Mediocre balance sheet low.

Similar Companies

Market Insights

Community Narratives