Returns On Capital At Lexus Granito (India) (NSE:LEXUS) Paint An Interesting Picture

If you're not sure where to start when looking for the next multi-bagger, there are a few key trends you should keep an eye out for. Firstly, we'll want to see a proven return on capital employed (ROCE) that is increasing, and secondly, an expanding base of capital employed. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. Although, when we looked at Lexus Granito (India) (NSE:LEXUS), it didn't seem to tick all of these boxes.

What is Return On Capital Employed (ROCE)?

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. To calculate this metric for Lexus Granito (India), this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

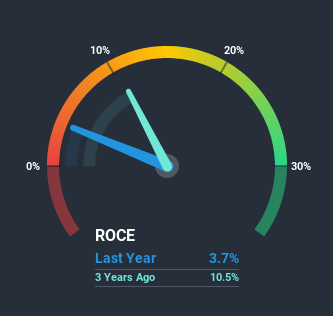

0.037 = ₹35m ÷ (₹1.8b - ₹885m) (Based on the trailing twelve months to March 2020).

So, Lexus Granito (India) has an ROCE of 3.7%. In absolute terms, that's a low return and it also under-performs the Consumer Durables industry average of 11%.

See our latest analysis for Lexus Granito (India)

Historical performance is a great place to start when researching a stock so above you can see the gauge for Lexus Granito (India)'s ROCE against it's prior returns. If you're interested in investigating Lexus Granito (India)'s past further, check out this free graph of past earnings, revenue and cash flow.

What Can We Tell From Lexus Granito (India)'s ROCE Trend?

On the surface, the trend of ROCE at Lexus Granito (India) doesn't inspire confidence. Around five years ago the returns on capital were 21%, but since then they've fallen to 3.7%. Given the business is employing more capital while revenue has slipped, this is a bit concerning. If this were to continue, you might be looking at a company that is trying to reinvest for growth but is actually losing market share since sales haven't increased.

On a side note, Lexus Granito (India)'s current liabilities are still rather high at 48% of total assets. This effectively means that suppliers (or short-term creditors) are funding a large portion of the business, so just be aware that this can introduce some elements of risk. Ideally we'd like to see this reduce as that would mean fewer obligations bearing risks.

In Conclusion...

In summary, we're somewhat concerned by Lexus Granito (India)'s diminishing returns on increasing amounts of capital. This could explain why the stock has sunk a total of 83% in the last three years. With underlying trends that aren't great in these areas, we'd consider looking elsewhere.

Since virtually every company faces some risks, it's worth knowing what they are, and we've spotted 4 warning signs for Lexus Granito (India) (of which 3 don't sit too well with us!) that you should know about.

While Lexus Granito (India) may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

When trading Lexus Granito (India) or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NSEI:LEXUS

Lexus Granito (India)

Engages in the manufacturing, trading, and marketing of vitrified ceramic and wall tiles under the LEXUS brand name in India and internationally.

Moderate and slightly overvalued.