Advertisement

What trends should we look for it we want to identify stocks that can multiply in value over the long term? One common approach is to try and find a company with returns on capital employed (ROCE) that are increasing, in conjunction with a growing amount of capital employed. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. With that in mind, the ROCE of Donear Industries (NSE:DONEAR) looks attractive right now, so lets see what the trend of returns can tell us.

Understanding Return On Capital Employed (ROCE)

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. To calculate this metric for Donear Industries, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

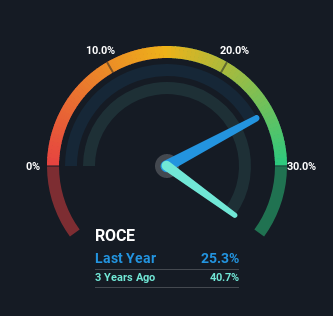

0.25 = ₹370m ÷ (₹5.3b - ₹3.9b) (Based on the trailing twelve months to December 2021).

Therefore, Donear Industries has an ROCE of 25%. In absolute terms that's a great return and it's even better than the Luxury industry average of 14%.

See our latest analysis for Donear Industries

Historical performance is a great place to start when researching a stock so above you can see the gauge for Donear Industries' ROCE against it's prior returns. If you're interested in investigating Donear Industries' past further, check out this free graph of past earnings, revenue and cash flow.

So How Is Donear Industries' ROCE Trending?

In terms of Donear Industries' history of ROCE, it's quite impressive. Over the past five years, ROCE has remained relatively flat at around 25% and the business has deployed 24% more capital into its operations. Returns like this are the envy of most businesses and given it has repeatedly reinvested at these rates, that's even better. If Donear Industries can keep this up, we'd be very optimistic about its future.

Another thing to note, Donear Industries has a high ratio of current liabilities to total assets of 73%. This can bring about some risks because the company is basically operating with a rather large reliance on its suppliers or other sorts of short-term creditors. While it's not necessarily a bad thing, it can be beneficial if this ratio is lower.

Our Take On Donear Industries' ROCE

Donear Industries has demonstrated its proficiency by generating high returns on increasing amounts of capital employed, which we're thrilled about. Yet over the last five years the stock has declined 31%, so the decline might provide an opening. That's why we think it'd be worthwhile to look further into this stock given the fundamentals are appealing.

One more thing: We've identified 5 warning signs with Donear Industries (at least 2 which don't sit too well with us) , and understanding these would certainly be useful.

If you want to search for more stocks that have been earning high returns, check out this free list of stocks with solid balance sheets that are also earning high returns on equity.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:DONEAR

Mediocre balance sheet and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|41.9% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|14.1% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$613.59|1.3% undervalued

AN

Based on Analyst Price Targets