Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, SecUR Credentials Limited (NSE:SECURCRED) does carry debt. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for SecUR Credentials

What Is SecUR Credentials's Net Debt?

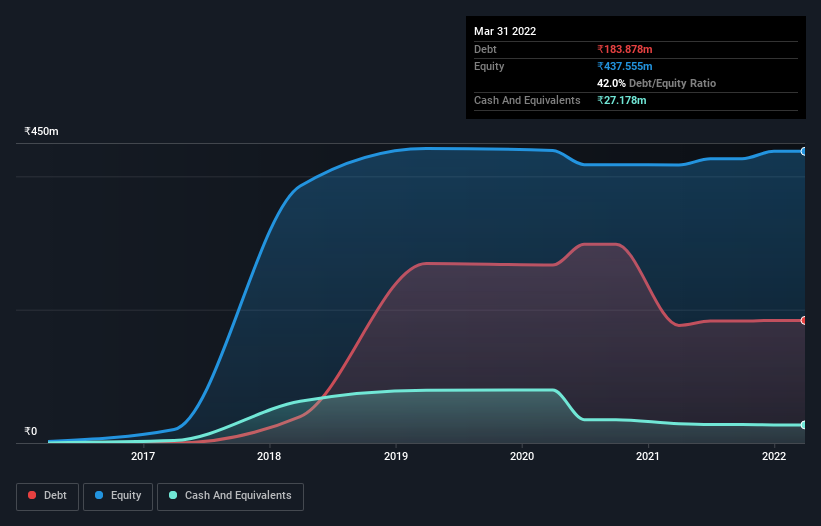

You can click the graphic below for the historical numbers, but it shows that as of March 2022 SecUR Credentials had ₹183.9m of debt, an increase on ₹176.4m, over one year. However, it does have ₹27.2m in cash offsetting this, leading to net debt of about ₹156.7m.

A Look At SecUR Credentials' Liabilities

According to the last reported balance sheet, SecUR Credentials had liabilities of ₹461.6m due within 12 months, and liabilities of ₹83.3m due beyond 12 months. Offsetting this, it had ₹27.2m in cash and ₹716.5m in receivables that were due within 12 months. So it actually has ₹198.9m more liquid assets than total liabilities.

This surplus liquidity suggests that SecUR Credentials' balance sheet could take a hit just as well as Homer Simpson's head can take a punch. With this in mind one could posit that its balance sheet means the company is able to handle some adversity.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Even though SecUR Credentials's debt is only 2.0, its interest cover is really very low at 2.5. This does suggest the company is paying fairly high interest rates. In any case, it's safe to say the company has meaningful debt. If SecUR Credentials can keep growing EBIT at last year's rate of 17% over the last year, then it will find its debt load easier to manage. When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since SecUR Credentials will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the last three years, SecUR Credentials reported free cash flow worth 8.5% of its EBIT, which is really quite low. For us, cash conversion that low sparks a little paranoia about is ability to extinguish debt.

Our View

The good news is that SecUR Credentials's demonstrated ability to handle its total liabilities delights us like a fluffy puppy does a toddler. But we must concede we find its interest cover has the opposite effect. Looking at all the aforementioned factors together, it strikes us that SecUR Credentials can handle its debt fairly comfortably. Of course, while this leverage can enhance returns on equity, it does bring more risk, so it's worth keeping an eye on this one. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. For instance, we've identified 4 warning signs for SecUR Credentials (2 don't sit too well with us) you should be aware of.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

If you're looking to trade SecUR Credentials, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:SECURCRED

SecUR Credentials

A background verification company, provides background screening and due diligence services in India.

Medium-low with mediocre balance sheet.