- India

- /

- Commercial Services

- /

- NSEI:KRYSTAL

Benign Growth For Krystal Integrated Services Limited (NSE:KRYSTAL) Underpins Stock's 26% Plummet

Krystal Integrated Services Limited (NSE:KRYSTAL) shareholders that were waiting for something to happen have been dealt a blow with a 26% share price drop in the last month. To make matters worse, the recent drop has wiped out a year's worth of gains with the share price now back where it started a year ago.

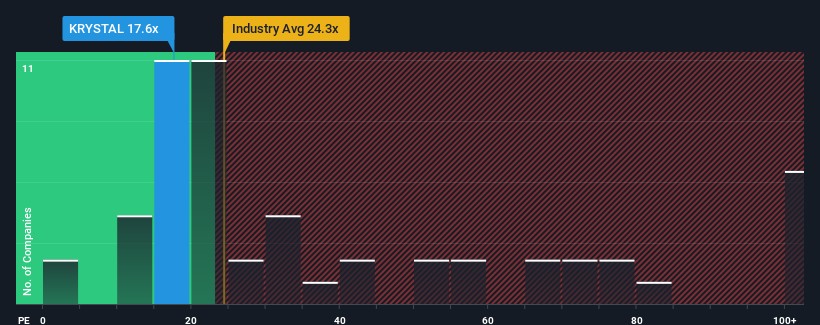

Following the heavy fall in price, given about half the companies in India have price-to-earnings ratios (or "P/E's") above 30x, you may consider Krystal Integrated Services as an attractive investment with its 17.6x P/E ratio. However, the P/E might be low for a reason and it requires further investigation to determine if it's justified.

As an illustration, earnings have deteriorated at Krystal Integrated Services over the last year, which is not ideal at all. One possibility is that the P/E is low because investors think the company won't do enough to avoid underperforming the broader market in the near future. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

View our latest analysis for Krystal Integrated Services

Is There Any Growth For Krystal Integrated Services?

The only time you'd be truly comfortable seeing a P/E as low as Krystal Integrated Services' is when the company's growth is on track to lag the market.

Retrospectively, the last year delivered a frustrating 7.2% decrease to the company's bottom line. Even so, admirably EPS has lifted 69% in aggregate from three years ago, notwithstanding the last 12 months. Accordingly, while they would have preferred to keep the run going, shareholders would probably welcome the medium-term rates of earnings growth.

Weighing that recent medium-term earnings trajectory against the broader market's one-year forecast for expansion of 25% shows it's noticeably less attractive on an annualised basis.

With this information, we can see why Krystal Integrated Services is trading at a P/E lower than the market. Apparently many shareholders weren't comfortable holding on to something they believe will continue to trail the bourse.

The Key Takeaway

Krystal Integrated Services' recently weak share price has pulled its P/E below most other companies. Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

As we suspected, our examination of Krystal Integrated Services revealed its three-year earnings trends are contributing to its low P/E, given they look worse than current market expectations. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. Unless the recent medium-term conditions improve, they will continue to form a barrier for the share price around these levels.

There are also other vital risk factors to consider before investing and we've discovered 2 warning signs for Krystal Integrated Services that you should be aware of.

You might be able to find a better investment than Krystal Integrated Services. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're here to simplify it.

Discover if Krystal Integrated Services might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:KRYSTAL

Krystal Integrated Services

Provides integrated facility management, staffing, payroll management, private security, manned guarding, and catering services in India.

Adequate balance sheet and slightly overvalued.

Similar Companies

Market Insights

Community Narratives