- India

- /

- Construction

- /

- NSEI:WELENT

Welspun Enterprises Limited (NSE:WELENT) Looks Inexpensive After Falling 26% But Perhaps Not Attractive Enough

Welspun Enterprises Limited (NSE:WELENT) shareholders won't be pleased to see that the share price has had a very rough month, dropping 26% and undoing the prior period's positive performance. Still, a bad month hasn't completely ruined the past year with the stock gaining 31%, which is great even in a bull market.

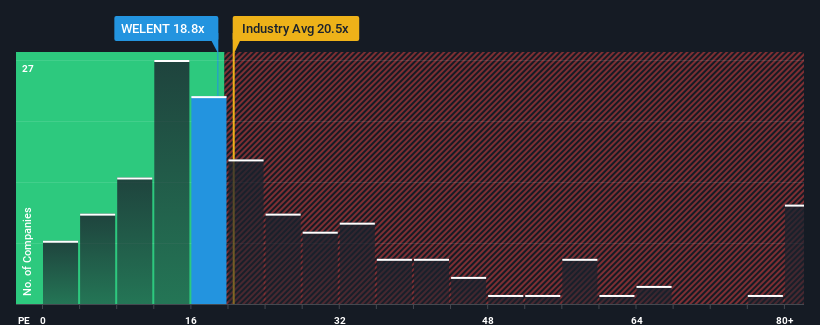

In spite of the heavy fall in price, Welspun Enterprises may still be sending bullish signals at the moment with its price-to-earnings (or "P/E") ratio of 18.8x, since almost half of all companies in India have P/E ratios greater than 27x and even P/E's higher than 51x are not unusual. However, the P/E might be low for a reason and it requires further investigation to determine if it's justified.

Welspun Enterprises could be doing better as its earnings have been going backwards lately while most other companies have been seeing positive earnings growth. It seems that many are expecting the dour earnings performance to persist, which has repressed the P/E. If you still like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

Check out our latest analysis for Welspun Enterprises

What Are Growth Metrics Telling Us About The Low P/E?

Welspun Enterprises' P/E ratio would be typical for a company that's only expected to deliver limited growth, and importantly, perform worse than the market.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 16%. Even so, admirably EPS has lifted 256% in aggregate from three years ago, notwithstanding the last 12 months. So we can start by confirming that the company has generally done a very good job of growing earnings over that time, even though it had some hiccups along the way.

Turning to the outlook, the next year should generate growth of 7.2% as estimated by the lone analyst watching the company. Meanwhile, the rest of the market is forecast to expand by 26%, which is noticeably more attractive.

In light of this, it's understandable that Welspun Enterprises' P/E sits below the majority of other companies. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

What We Can Learn From Welspun Enterprises' P/E?

Welspun Enterprises' recently weak share price has pulled its P/E below most other companies. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

We've established that Welspun Enterprises maintains its low P/E on the weakness of its forecast growth being lower than the wider market, as expected. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

And what about other risks? Every company has them, and we've spotted 2 warning signs for Welspun Enterprises you should know about.

If these risks are making you reconsider your opinion on Welspun Enterprises, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Welspun Enterprises might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:WELENT

Welspun Enterprises

Engages in the engineering, procurement, and construction of infrastructure development projects in India.

Excellent balance sheet and slightly overvalued.

Similar Companies

Market Insights

Community Narratives