- India

- /

- Electrical

- /

- NSEI:VMARCIND

Insiders still control 70% of V-MARC India Limited (NSE:VMARCIND) despite recent sales

Key Insights

- V-MARC India's significant insider ownership suggests inherent interests in company's expansion

- 55% of the company is held by a single shareholder (Vikas Garg)

- Insiders have sold recently

If you want to know who really controls V-MARC India Limited (NSE:VMARCIND), then you'll have to look at the makeup of its share registry. The group holding the most number of shares in the company, around 70% to be precise, is individual insiders. In other words, the group stands to gain the most (or lose the most) from their investment into the company.

Insiders are at the top of the company's shareholdings despite selling some shares recently. As a result, they were also the biggest winners as market cap hit ₹9.5b last week.

In the chart below, we zoom in on the different ownership groups of V-MARC India.

View our latest analysis for V-MARC India

What Does The Lack Of Institutional Ownership Tell Us About V-MARC India?

We don't tend to see institutional investors holding stock of companies that are very risky, thinly traded, or very small. Though we do sometimes see large companies without institutions on the register, it's not particularly common.

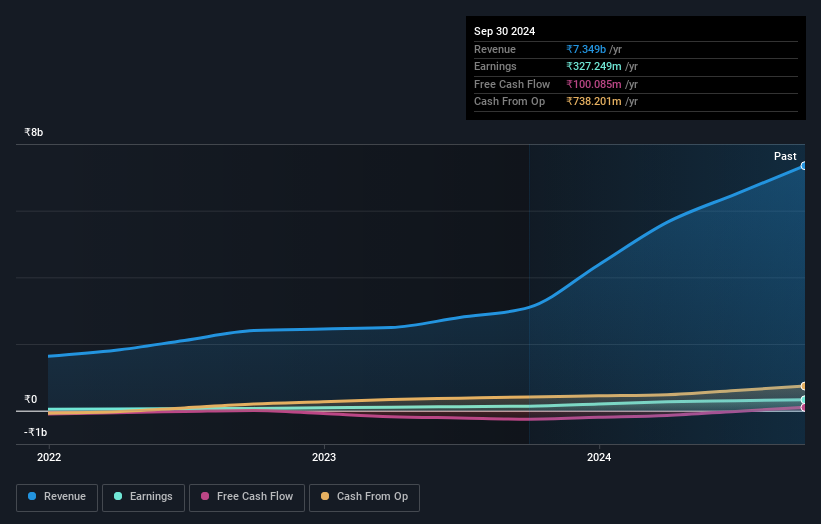

There could be various reasons why no institutions own shares in a company. Typically, small, newly listed companies don't attract much attention from fund managers, because it would not be possible for large fund managers to build a meaningful position in the company. It is also possible that fund managers don't own the stock because they aren't convinced it will perform well. V-MARC India's earnings and revenue track record (below) may not be compelling to institutional investors -- or they simply might not have looked at the business closely.

V-MARC India is not owned by hedge funds. With a 55% stake, CEO Vikas Garg is the largest shareholder. This implies that they possess majority interests and have significant control over the company. Investors usually consider it a good sign when the company leadership has such a significant stake, as this is widely perceived to increase the chance that the management will act in the best interests of the company. Meanwhile, the second and third largest shareholders, hold 14% and 0.04%, of the shares outstanding, respectively. Interestingly, the third-largest shareholder, Deepak Tikle is also a Member of the Board of Directors, again, indicating strong insider ownership amongst the company's top shareholders.

While studying institutional ownership for a company can add value to your research, it is also a good practice to research analyst recommendations to get a deeper understand of a stock's expected performance. We're not picking up on any analyst coverage of the stock at the moment, so the company is unlikely to be widely held.

Insider Ownership Of V-MARC India

The definition of company insiders can be subjective and does vary between jurisdictions. Our data reflects individual insiders, capturing board members at the very least. The company management answer to the board and the latter should represent the interests of shareholders. Notably, sometimes top-level managers are on the board themselves.

I generally consider insider ownership to be a good thing. However, on some occasions it makes it more difficult for other shareholders to hold the board accountable for decisions.

Our most recent data indicates that insiders own the majority of V-MARC India Limited. This means they can collectively make decisions for the company. That means they own ₹6.6b worth of shares in the ₹9.5b company. That's quite meaningful. It is good to see this level of investment. You can check here to see if those insiders have been buying recently.

General Public Ownership

The general public, who are usually individual investors, hold a 30% stake in V-MARC India. While this group can't necessarily call the shots, it can certainly have a real influence on how the company is run.

Next Steps:

While it is well worth considering the different groups that own a company, there are other factors that are even more important. Case in point: We've spotted 2 warning signs for V-MARC India you should be aware of, and 1 of them is a bit concerning.

If you would prefer check out another company -- one with potentially superior financials -- then do not miss this free list of interesting companies, backed by strong financial data.

NB: Figures in this article are calculated using data from the last twelve months, which refer to the 12-month period ending on the last date of the month the financial statement is dated. This may not be consistent with full year annual report figures.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:VMARCIND

V-MARC India

Manufactures and markets electrical wires and cables under the V-Marc brand name in India.

Solid track record with mediocre balance sheet.

Similar Companies

Market Insights

Community Narratives