- India

- /

- Electrical

- /

- NSEI:SWELECTES

Swelect Energy Systems (NSE:SWELECTES) Has Announced That It Will Be Increasing Its Dividend To ₹4.00

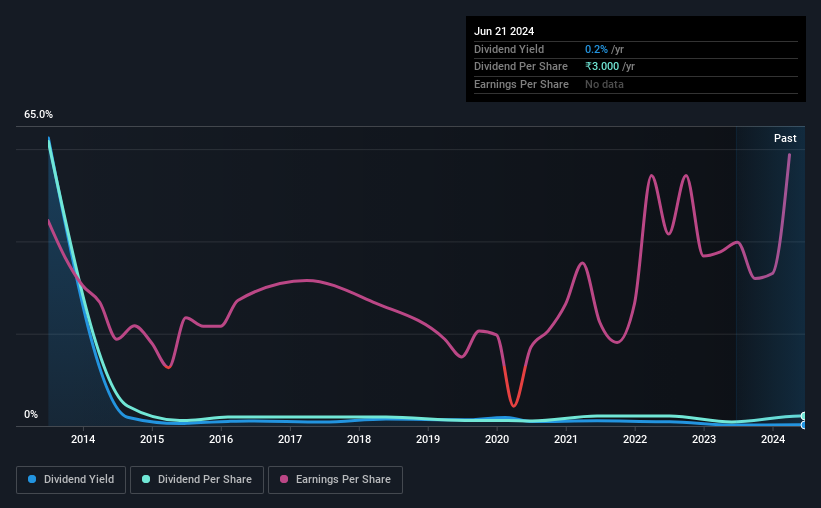

Swelect Energy Systems Limited (NSE:SWELECTES) has announced that it will be increasing its dividend from last year's comparable payment on the 9th of August to ₹4.00. Even though the dividend went up, the yield is still quite low at only 0.2%.

While the dividend yield is important for income investors, it is also important to consider any large share price moves, as this will generally outweigh any gains from distributions. Investors will be pleased to see that Swelect Energy Systems' stock price has increased by 40% in the last 3 months, which is good for shareholders and can also explain a decrease in the dividend yield.

Check out our latest analysis for Swelect Energy Systems

Swelect Energy Systems' Dividend Is Well Covered By Earnings

While yield is important, another factor to consider about a company's dividend is whether the current payout levels are feasible. Swelect Energy Systems is quite easily earning enough to cover the dividend, however it is being let down by weak cash flows. We think that cash flows should take priority over earnings, so this is definitely a worry for the dividend going forward.

If the trend of the last few years continues, EPS will grow by 50.4% over the next 12 months. Assuming the dividend continues along recent trends, we think the payout ratio could be 7.2% by next year, which is in a pretty sustainable range.

Dividend Volatility

The company's dividend history has been marked by instability, with at least one cut in the last 10 years. Since 2014, the annual payment back then was ₹85.33, compared to the most recent full-year payment of ₹3.00. Dividend payments have fallen sharply, down 96% over that time. Generally, we don't like to see a dividend that has been declining over time as this can degrade shareholders' returns and indicate that the company may be running into problems.

The Dividend Looks Likely To Grow

Given that dividend payments have been shrinking like a glacier in a warming world, we need to check if there are some bright spots on the horizon. We are encouraged to see that Swelect Energy Systems has grown earnings per share at 50% per year over the past five years. A low payout ratio gives the company a lot of flexibility, and growing earnings also make it very easy for it to grow the dividend.

Our Thoughts On Swelect Energy Systems' Dividend

Overall, we always like to see the dividend being raised, but we don't think Swelect Energy Systems will make a great income stock. With cash flows lacking, it is difficult to see how the company can sustain a dividend payment. We would probably look elsewhere for an income investment.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. As an example, we've identified 2 warning signs for Swelect Energy Systems that you should be aware of before investing. Is Swelect Energy Systems not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NSEI:SWELECTES

Swelect Energy Systems

Engages in the manufacture and trading of solar modules, mounting structures, transformers, and inverters in India, Europe, and internationally.

Proven track record with mediocre balance sheet.