Advertisement

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Swelect Energy Systems Limited (NSE:SWELECTES) does use debt in its business. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Swelect Energy Systems

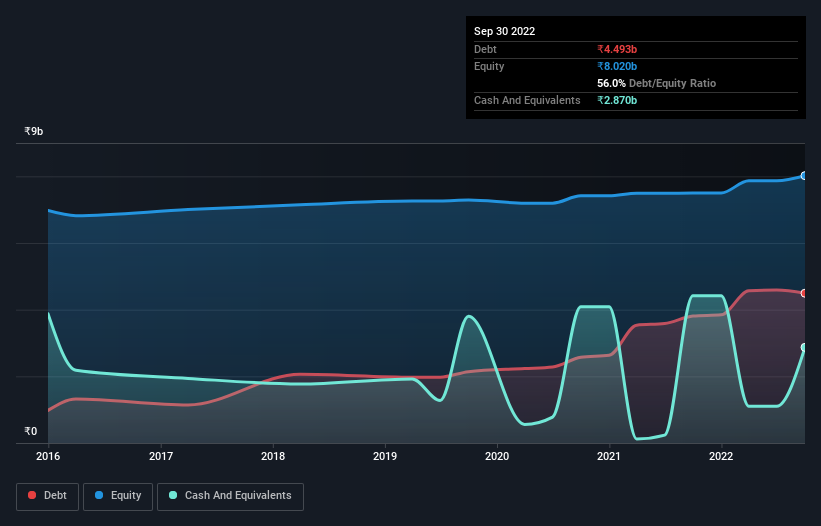

How Much Debt Does Swelect Energy Systems Carry?

The image below, which you can click on for greater detail, shows that at September 2022 Swelect Energy Systems had debt of ₹4.49b, up from ₹3.81b in one year. However, because it has a cash reserve of ₹2.87b, its net debt is less, at about ₹1.62b.

How Strong Is Swelect Energy Systems' Balance Sheet?

We can see from the most recent balance sheet that Swelect Energy Systems had liabilities of ₹3.49b falling due within a year, and liabilities of ₹2.03b due beyond that. On the other hand, it had cash of ₹2.87b and ₹851.2m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by ₹1.80b.

Swelect Energy Systems has a market capitalization of ₹4.65b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Swelect Energy Systems has net debt worth 1.7 times EBITDA, which isn't too much, but its interest cover looks a bit on the low side, with EBIT at only 3.5 times the interest expense. While these numbers do not alarm us, it's worth noting that the cost of the company's debt is having a real impact. Notably, Swelect Energy Systems's EBIT launched higher than Elon Musk, gaining a whopping 385% on last year. There's no doubt that we learn most about debt from the balance sheet. But it is Swelect Energy Systems's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So it's worth checking how much of that EBIT is backed by free cash flow. Over the last three years, Swelect Energy Systems saw substantial negative free cash flow, in total. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

Swelect Energy Systems's conversion of EBIT to free cash flow and interest cover definitely weigh on it, in our esteem. But its EBIT growth rate tells a very different story, and suggests some resilience. We think that Swelect Energy Systems's debt does make it a bit risky, after considering the aforementioned data points together. Not all risk is bad, as it can boost share price returns if it pays off, but this debt risk is worth keeping in mind. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. We've identified 3 warning signs with Swelect Energy Systems , and understanding them should be part of your investment process.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:SWELECTES

Swelect Energy Systems

Engages in the manufacture and trading of solar mounting structures, solar photovoltaic inverters**and other ancillary products in India.

Moderate risk with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Quality at a Premium. A time to watch, not to buy?

Fair Value US$154.56|29.3% undervalued

DA

Community Contributor

GRAB: The Super-App at the Heart of Southeast Asia’s Digital Boom

Fair Value US$6.60|7.0% undervalued

BL

Community Contributor

Verve Group to Surge with 51.61% Revenue Growth

Fair Value €6.00|65.0% undervalued

ME

Community Contributor