- India

- /

- Electrical

- /

- NSEI:SUZLON

Why We're Not Concerned About Suzlon Energy Limited's (NSE:SUZLON) Share Price

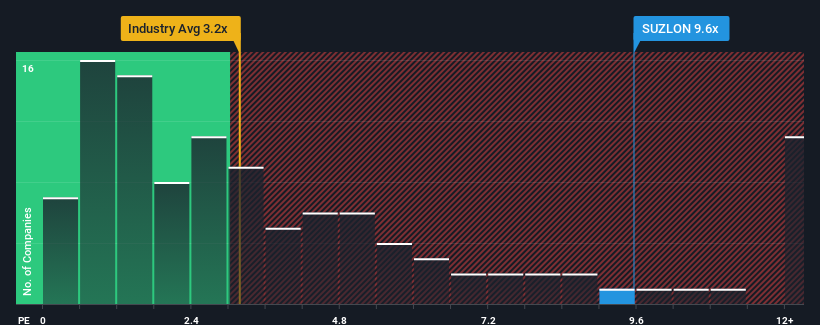

When close to half the companies in the Electrical industry in India have price-to-sales ratios (or "P/S") below 3.2x, you may consider Suzlon Energy Limited (NSE:SUZLON) as a stock to avoid entirely with its 9.6x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/S.

Check out our latest analysis for Suzlon Energy

What Does Suzlon Energy's Recent Performance Look Like?

Suzlon Energy hasn't been tracking well recently as its declining revenue compares poorly to other companies, which have seen some growth in their revenues on average. Perhaps the market is expecting the poor revenue to reverse, justifying it's current high P/S.. However, if this isn't the case, investors might get caught out paying too much for the stock.

Keen to find out how analysts think Suzlon Energy's future stacks up against the industry? In that case, our free report is a great place to start.How Is Suzlon Energy's Revenue Growth Trending?

There's an inherent assumption that a company should far outperform the industry for P/S ratios like Suzlon Energy's to be considered reasonable.

In reviewing the last year of financials, we were disheartened to see the company's revenues fell to the tune of 10%. However, a few very strong years before that means that it was still able to grow revenue by an impressive 113% in total over the last three years. So we can start by confirming that the company has generally done a very good job of growing revenue over that time, even though it had some hiccups along the way.

Turning to the outlook, the next year should generate growth of 80% as estimated by the three analysts watching the company. That's shaping up to be materially higher than the 30% growth forecast for the broader industry.

With this information, we can see why Suzlon Energy is trading at such a high P/S compared to the industry. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Key Takeaway

Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

As we suspected, our examination of Suzlon Energy's analyst forecasts revealed that its superior revenue outlook is contributing to its high P/S. At this stage investors feel the potential for a deterioration in revenues is quite remote, justifying the elevated P/S ratio. It's hard to see the share price falling strongly in the near future under these circumstances.

You always need to take note of risks, for example - Suzlon Energy has 3 warning signs we think you should be aware of.

If these risks are making you reconsider your opinion on Suzlon Energy, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:SUZLON

Suzlon Energy

Manufactures and sells wind turbine generators and related components in India and internationally.

Exceptional growth potential with outstanding track record.