- India

- /

- Electrical

- /

- NSEI:SCHNEIDER

Subdued Growth No Barrier To Schneider Electric Infrastructure Limited (NSE:SCHNEIDER) With Shares Advancing 25%

Despite an already strong run, Schneider Electric Infrastructure Limited (NSE:SCHNEIDER) shares have been powering on, with a gain of 25% in the last thirty days. This latest share price bounce rounds out a remarkable 309% gain over the last twelve months.

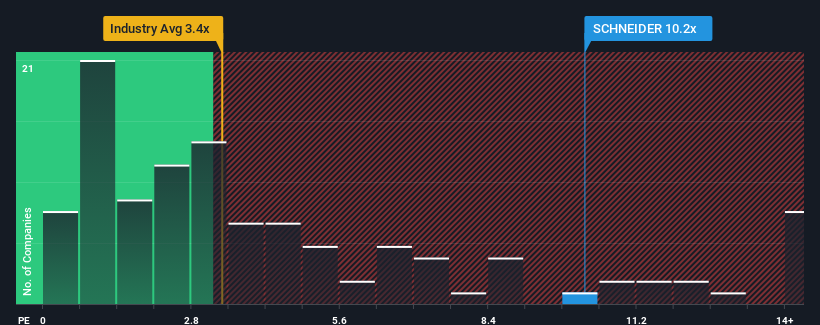

After such a large jump in price, given around half the companies in India's Electrical industry have price-to-sales ratios (or "P/S") below 3.4x, you may consider Schneider Electric Infrastructure as a stock to avoid entirely with its 10.2x P/S ratio. However, the P/S might be quite high for a reason and it requires further investigation to determine if it's justified.

See our latest analysis for Schneider Electric Infrastructure

What Does Schneider Electric Infrastructure's Recent Performance Look Like?

Schneider Electric Infrastructure has been doing a good job lately as it's been growing revenue at a solid pace. One possibility is that the P/S ratio is high because investors think this respectable revenue growth will be enough to outperform the broader industry in the near future. However, if this isn't the case, investors might get caught out paying too much for the stock.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on Schneider Electric Infrastructure will help you shine a light on its historical performance.How Is Schneider Electric Infrastructure's Revenue Growth Trending?

Schneider Electric Infrastructure's P/S ratio would be typical for a company that's expected to deliver very strong growth, and importantly, perform much better than the industry.

If we review the last year of revenue growth, the company posted a terrific increase of 26%. Pleasingly, revenue has also lifted 67% in aggregate from three years ago, thanks to the last 12 months of growth. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Comparing that to the industry, which is predicted to deliver 30% growth in the next 12 months, the company's momentum is weaker, based on recent medium-term annualised revenue results.

In light of this, it's alarming that Schneider Electric Infrastructure's P/S sits above the majority of other companies. Apparently many investors in the company are way more bullish than recent times would indicate and aren't willing to let go of their stock at any price. Only the boldest would assume these prices are sustainable as a continuation of recent revenue trends is likely to weigh heavily on the share price eventually.

The Key Takeaway

Schneider Electric Infrastructure's P/S has grown nicely over the last month thanks to a handy boost in the share price. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

Our examination of Schneider Electric Infrastructure revealed its poor three-year revenue trends aren't detracting from the P/S as much as we though, given they look worse than current industry expectations. When we see slower than industry revenue growth but an elevated P/S, there's considerable risk of the share price declining, sending the P/S lower. If recent medium-term revenue trends continue, it will place shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

Before you settle on your opinion, we've discovered 1 warning sign for Schneider Electric Infrastructure that you should be aware of.

If these risks are making you reconsider your opinion on Schneider Electric Infrastructure, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:SCHNEIDER

Schneider Electric Infrastructure

Designs, manufactures, builds, and services products and systems for electricity distribution in India and internationally.

Excellent balance sheet with limited growth.

Market Insights

Community Narratives