- India

- /

- Construction

- /

- NSEI:OMINFRAL

These 4 Measures Indicate That Om Infra (NSE:OMINFRAL) Is Using Debt Extensively

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that Om Infra Limited (NSE:OMINFRAL) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for Om Infra

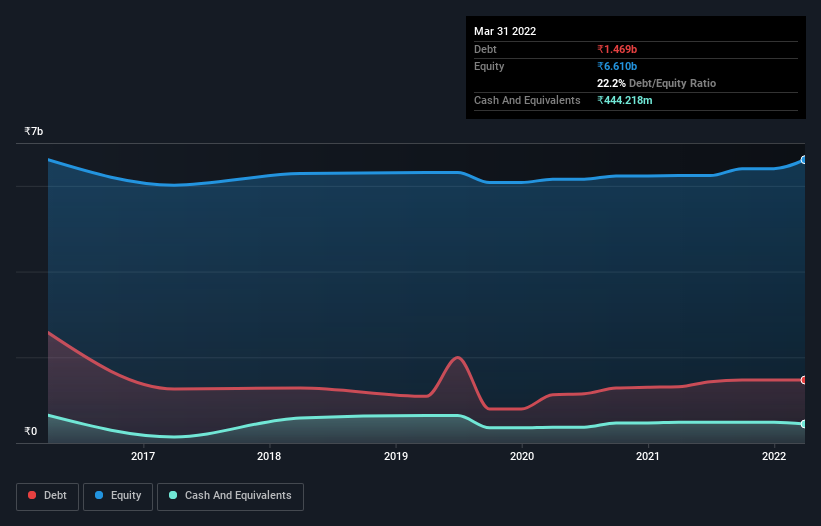

How Much Debt Does Om Infra Carry?

As you can see below, at the end of March 2022, Om Infra had ₹1.47b of debt, up from ₹1.31b a year ago. Click the image for more detail. However, it also had ₹444.2m in cash, and so its net debt is ₹1.03b.

How Strong Is Om Infra's Balance Sheet?

According to the last reported balance sheet, Om Infra had liabilities of ₹4.48b due within 12 months, and liabilities of ₹901.2m due beyond 12 months. On the other hand, it had cash of ₹444.2m and ₹2.01b worth of receivables due within a year. So it has liabilities totalling ₹2.93b more than its cash and near-term receivables, combined.

This deficit is considerable relative to its market capitalization of ₹3.11b, so it does suggest shareholders should keep an eye on Om Infra's use of debt. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

While Om Infra has a quite reasonable net debt to EBITDA multiple of 2.3, its interest cover seems weak, at 1.0. This does suggest the company is paying fairly high interest rates. In any case, it's safe to say the company has meaningful debt. Unfortunately, Om Infra saw its EBIT slide 9.7% in the last twelve months. If earnings continue on that decline then managing that debt will be difficult like delivering hot soup on a unicycle. The balance sheet is clearly the area to focus on when you are analysing debt. But it is Om Infra's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the last three years, Om Infra barely recorded positive free cash flow, in total. Some might say that's a concern, when it comes considering how easily it would be for it to down debt.

Our View

Mulling over Om Infra's attempt at covering its interest expense with its EBIT, we're certainly not enthusiastic. But at least its net debt to EBITDA is not so bad. We're quite clear that we consider Om Infra to be really rather risky, as a result of its balance sheet health. For this reason we're pretty cautious about the stock, and we think shareholders should keep a close eye on its liquidity. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. To that end, you should learn about the 4 warning signs we've spotted with Om Infra (including 1 which is concerning) .

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:OMINFRAL

Om Infra

Engages in the design, engineering, manufacture, supply, installation, testing, and commissioning of hydro mechanical equipment for hydroelectric power and irrigation projects in India and internationally.

Excellent balance sheet average dividend payer.