Advertisement

Olectra Greentech (NSE:OLECTRA) Seems To Use Debt Quite Sensibly

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Olectra Greentech Limited (NSE:OLECTRA) does use debt in its business. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Olectra Greentech

What Is Olectra Greentech's Debt?

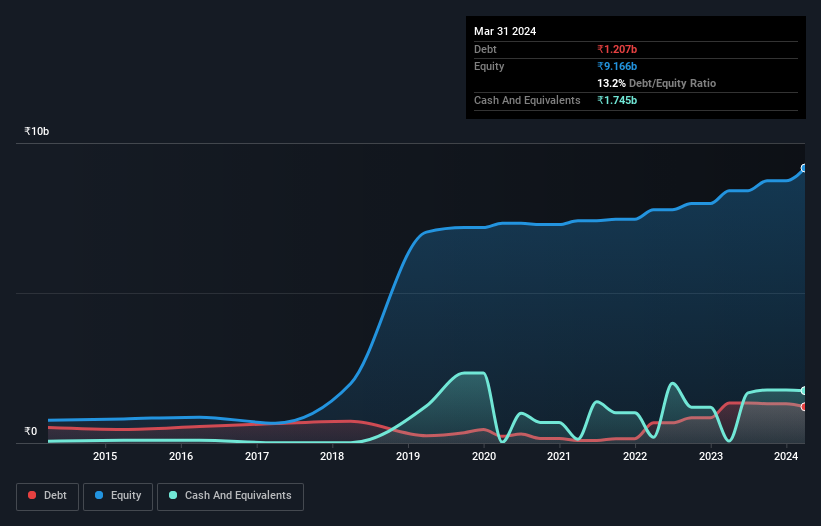

You can click the graphic below for the historical numbers, but it shows that Olectra Greentech had ₹1.21b of debt in March 2024, down from ₹1.34b, one year before. However, its balance sheet shows it holds ₹1.75b in cash, so it actually has ₹537.9m net cash.

How Healthy Is Olectra Greentech's Balance Sheet?

The latest balance sheet data shows that Olectra Greentech had liabilities of ₹6.14b due within a year, and liabilities of ₹583.2m falling due after that. On the other hand, it had cash of ₹1.75b and ₹5.54b worth of receivables due within a year. So it can boast ₹562.0m more liquid assets than total liabilities.

This state of affairs indicates that Olectra Greentech's balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So while it's hard to imagine that the ₹127.9b company is struggling for cash, we still think it's worth monitoring its balance sheet. Simply put, the fact that Olectra Greentech has more cash than debt is arguably a good indication that it can manage its debt safely.

One way Olectra Greentech could vanquish its debt would be if it stops borrowing more but continues to grow EBIT at around 19%, as it did over the last year. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Olectra Greentech can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. While Olectra Greentech has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Over the last three years, Olectra Greentech reported free cash flow worth 15% of its EBIT, which is really quite low. That limp level of cash conversion undermines its ability to manage and pay down debt.

Summing Up

While we empathize with investors who find debt concerning, you should keep in mind that Olectra Greentech has net cash of ₹537.9m, as well as more liquid assets than liabilities. And we liked the look of last year's 19% year-on-year EBIT growth. So we are not troubled with Olectra Greentech's debt use. Over time, share prices tend to follow earnings per share, so if you're interested in Olectra Greentech, you may well want to click here to check an interactive graph of its earnings per share history.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NSEI:OLECTRA

Olectra Greentech

Manufactures and sells electric buses and trucks in India.

High growth potential with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.4% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|6.1% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.2% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor