Advertisement

We Think Shareholders Are Less Likely To Approve A Large Pay Rise For Lakshmi Machine Works Limited's (NSE:LAXMIMACH) CEO For Now

Key Insights

- Lakshmi Machine Works will host its Annual General Meeting on 31st of July

- Salary of ₹19.4m is part of CEO Sanjay Jayavarthanavelu's total remuneration

- The total compensation is 477% higher than the average for the industry

- Over the past three years, Lakshmi Machine Works' EPS grew by 103% and over the past three years, the total shareholder return was 98%

Performance at Lakshmi Machine Works Limited (NSE:LAXMIMACH) has been reasonably good and CEO Sanjay Jayavarthanavelu has done a decent job of steering the company in the right direction. As shareholders go into the upcoming AGM on 31st of July, CEO compensation will probably not be their focus, but rather the steps management will take to continue the growth momentum. However, some shareholders may still be hesitant of being overly generous with CEO compensation.

See our latest analysis for Lakshmi Machine Works

How Does Total Compensation For Sanjay Jayavarthanavelu Compare With Other Companies In The Industry?

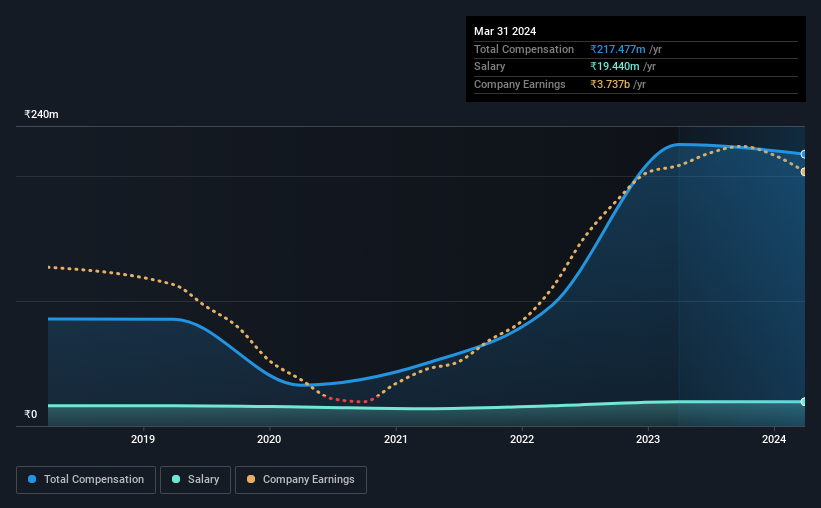

Our data indicates that Lakshmi Machine Works Limited has a market capitalization of ₹167b, and total annual CEO compensation was reported as ₹217m for the year to March 2024. That's slightly lower by 3.5% over the previous year. We think total compensation is more important but our data shows that the CEO salary is lower, at ₹19m.

For comparison, other companies in the Indian Machinery industry with market capitalizations ranging between ₹84b and ₹268b had a median total CEO compensation of ₹38m. Accordingly, our analysis reveals that Lakshmi Machine Works Limited pays Sanjay Jayavarthanavelu north of the industry median. Moreover, Sanjay Jayavarthanavelu also holds ₹2.2b worth of Lakshmi Machine Works stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | ₹19m | ₹19m | 9% |

| Other | ₹198m | ₹206m | 91% |

| Total Compensation | ₹217m | ₹225m | 100% |

Speaking on an industry level, nearly 92% of total compensation represents salary, while the remainder of 8% is other remuneration. Lakshmi Machine Works sets aside a smaller share of compensation for salary, in comparison to the overall industry. If non-salary compensation dominates total pay, it's an indicator that the executive's salary is tied to company performance.

Lakshmi Machine Works Limited's Growth

Lakshmi Machine Works Limited has seen its earnings per share (EPS) increase by 103% a year over the past three years. In the last year, its revenue changed by just 0.4%.

Overall this is a positive result for shareholders, showing that the company has improved in recent years. While it would be good to see revenue growth, profits matter more in the end. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has Lakshmi Machine Works Limited Been A Good Investment?

We think that the total shareholder return of 98%, over three years, would leave most Lakshmi Machine Works Limited shareholders smiling. As a result, some may believe the CEO should be paid more than is normal for companies of similar size.

In Summary...

Given that the company's overall performance has been reasonable, the CEO remuneration policy might not be shareholders' central point of focus in the upcoming AGM. However, any decision to raise CEO pay might be met with some objections from the shareholders given that the CEO is already paid higher than the industry average.

CEO pay is simply one of the many factors that need to be considered while examining business performance. We identified 2 warning signs for Lakshmi Machine Works (1 is a bit concerning!) that you should be aware of before investing here.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NSEI:LMW

LMW

Manufactures and sells textile spinning machinery in India and internationally.

Flawless balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

50 followersusers have followed this narrative

6 commentsusers have commented on this narrative

16 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

MO

mo7md on ADNOC Gas ·

ADNOC Gas future shines with a 21.4% revenue surge

Fair Value:د.إ3.728.9% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

IN

IncomeAssets on Pulse Seismic ·

Watch Pulse Seismic Outperform with 13.6% Revenue Growth in the Coming Years

Fair Value:CA$4.4727.3% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$481.5% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.2% undervalued

957 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

50 followersusers have followed this narrative

6 commentsusers have commented on this narrative

16 likesusers have liked this narrative