- India

- /

- Construction

- /

- NSEI:KCEIL

Kay Cee Energy & Infra Limited's (NSE:KCEIL) Stock Retreats 26% But Earnings Haven't Escaped The Attention Of Investors

Kay Cee Energy & Infra Limited (NSE:KCEIL) shares have had a horrible month, losing 26% after a relatively good period beforehand. Longer-term shareholders will rue the drop in the share price, since it's now virtually flat for the year after a promising few quarters.

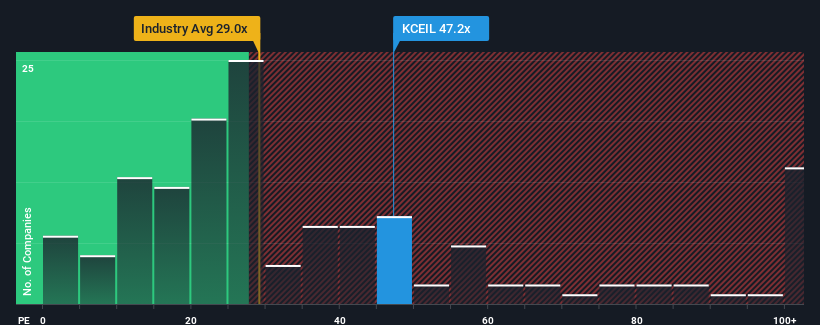

Although its price has dipped substantially, Kay Cee Energy & Infra's price-to-earnings (or "P/E") ratio of 47.2x might still make it look like a sell right now compared to the market in India, where around half of the companies have P/E ratios below 33x and even P/E's below 19x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/E.

Kay Cee Energy & Infra has been doing a decent job lately as it's been growing earnings at a reasonable pace. It might be that many expect the reasonable earnings performance to beat most other companies over the coming period, which has increased investors’ willingness to pay up for the stock. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Check out our latest analysis for Kay Cee Energy & Infra

How Is Kay Cee Energy & Infra's Growth Trending?

Kay Cee Energy & Infra's P/E ratio would be typical for a company that's expected to deliver solid growth, and importantly, perform better than the market.

Taking a look back first, we see that the company managed to grow earnings per share by a handy 7.1% last year. Pleasingly, EPS has also lifted 147% in aggregate from three years ago, partly thanks to the last 12 months of growth. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Comparing that to the market, which is only predicted to deliver 26% growth in the next 12 months, the company's momentum is stronger based on recent medium-term annualised earnings results.

In light of this, it's understandable that Kay Cee Energy & Infra's P/E sits above the majority of other companies. It seems most investors are expecting this strong growth to continue and are willing to pay more for the stock.

The Bottom Line On Kay Cee Energy & Infra's P/E

Despite the recent share price weakness, Kay Cee Energy & Infra's P/E remains higher than most other companies. Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that Kay Cee Energy & Infra maintains its high P/E on the strength of its recent three-year growth being higher than the wider market forecast, as expected. Right now shareholders are comfortable with the P/E as they are quite confident earnings aren't under threat. Unless the recent medium-term conditions change, they will continue to provide strong support to the share price.

Before you take the next step, you should know about the 4 warning signs for Kay Cee Energy & Infra (2 make us uncomfortable!) that we have uncovered.

Of course, you might also be able to find a better stock than Kay Cee Energy & Infra. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're here to simplify it.

Discover if Kay Cee Energy & Infra might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:KCEIL

Kay Cee Energy & Infra

Engages in the infrastructure development for power transmission and distribution system industries in India.

Moderate with acceptable track record.

Similar Companies

Market Insights

Community Narratives