Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Inox Wind Limited (NSE:INOXWIND) does carry debt. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Inox Wind

What Is Inox Wind's Net Debt?

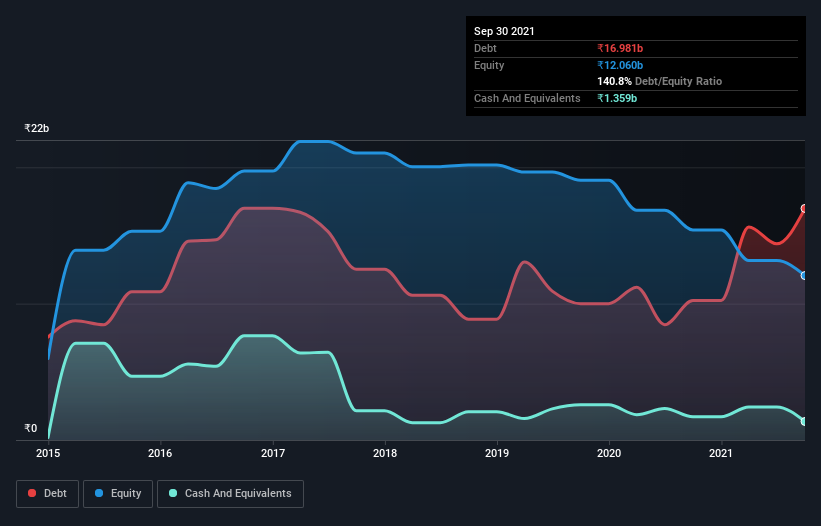

As you can see below, at the end of September 2021, Inox Wind had ₹17.0b of debt, up from ₹10.2b a year ago. Click the image for more detail. However, because it has a cash reserve of ₹1.36b, its net debt is less, at about ₹15.6b.

A Look At Inox Wind's Liabilities

According to the last reported balance sheet, Inox Wind had liabilities of ₹38.8b due within 12 months, and liabilities of ₹4.95b due beyond 12 months. Offsetting this, it had ₹1.36b in cash and ₹10.7b in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by ₹31.7b.

When you consider that this deficiency exceeds the company's ₹28.6b market capitalization, you might well be inclined to review the balance sheet intently. Hypothetically, extremely heavy dilution would be required if the company were forced to pay down its liabilities by raising capital at the current share price. When analysing debt levels, the balance sheet is the obvious place to start. But it is Inox Wind's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

In the last year Inox Wind wasn't profitable at an EBIT level, but managed to grow its revenue by 24%, to ₹7.8b. Shareholders probably have their fingers crossed that it can grow its way to profits.

Caveat Emptor

Even though Inox Wind managed to grow its top line quite deftly, the cold hard truth is that it is losing money on the EBIT line. To be specific the EBIT loss came in at ₹1.8b. Considering that alongside the liabilities mentioned above make us nervous about the company. It would need to improve its operations quickly for us to be interested in it. Not least because it burned through ₹3.4b in negative free cash flow over the last year. That means it's on the risky side of things. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. Case in point: We've spotted 3 warning signs for Inox Wind you should be aware of, and 2 of them are a bit concerning.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NSEI:INOXWIND

Inox Wind

Engages in the manufacture and sale of wind turbine generators and components for independent power producers, utilities, public sector undertakings, businesses, and private investors in India.

Exceptional growth potential and fair value.

Similar Companies

Market Insights

Community Narratives