- India

- /

- Electrical

- /

- NSEI:HAVELLS

Havells India Limited's (NSE:HAVELLS) Price Is Out Of Tune With Revenues

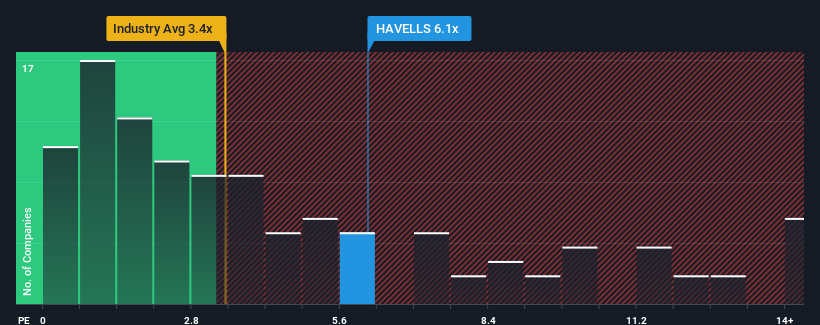

When you see that almost half of the companies in the Electrical industry in India have price-to-sales ratios (or "P/S") below 3.4x, Havells India Limited (NSE:HAVELLS) looks to be giving off strong sell signals with its 6.1x P/S ratio. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so lofty.

See our latest analysis for Havells India

What Does Havells India's Recent Performance Look Like?

Havells India could be doing better as it's been growing revenue less than most other companies lately. One possibility is that the P/S ratio is high because investors think this lacklustre revenue performance will improve markedly. However, if this isn't the case, investors might get caught out paying too much for the stock.

Want the full picture on analyst estimates for the company? Then our free report on Havells India will help you uncover what's on the horizon.How Is Havells India's Revenue Growth Trending?

There's an inherent assumption that a company should far outperform the industry for P/S ratios like Havells India's to be considered reasonable.

Taking a look back first, we see that the company managed to grow revenues by a handy 9.9% last year. This was backed up an excellent period prior to see revenue up by 78% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Looking ahead now, revenue is anticipated to climb by 14% each year during the coming three years according to the analysts following the company. That's shaping up to be materially lower than the 22% per year growth forecast for the broader industry.

With this information, we find it concerning that Havells India is trading at a P/S higher than the industry. Apparently many investors in the company are way more bullish than analysts indicate and aren't willing to let go of their stock at any price. There's a good chance these shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with the growth outlook.

The Final Word

Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

It comes as a surprise to see Havells India trade at such a high P/S given the revenue forecasts look less than stellar. When we see a weak revenue outlook, we suspect the share price faces a much greater risk of declining, bringing back down the P/S figures. This places shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

There are also other vital risk factors to consider before investing and we've discovered 1 warning sign for Havells India that you should be aware of.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're here to simplify it.

Discover if Havells India might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NSEI:HAVELLS

Havells India

A fast-moving electrical goods company, manufactures, trades in, and sells various consumer electrical and electronic products in India and internationally.

Excellent balance sheet with reasonable growth potential and pays a dividend.