- India

- /

- Aerospace & Defense

- /

- NSEI:GRSE

Garden Reach Shipbuilders & Engineers Limited (NSE:GRSE) May Have Run Too Fast Too Soon With Recent 28% Price Plummet

The Garden Reach Shipbuilders & Engineers Limited (NSE:GRSE) share price has softened a substantial 28% over the previous 30 days, handing back much of the gains the stock has made lately. The good news is that in the last year, the stock has shone bright like a diamond, gaining 133%.

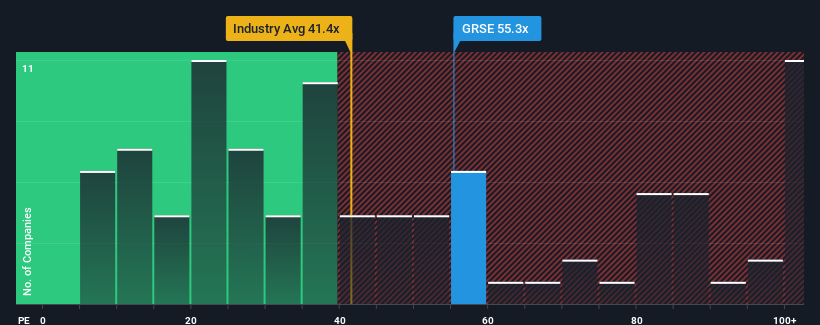

In spite of the heavy fall in price, Garden Reach Shipbuilders & Engineers may still be sending very bearish signals at the moment with a price-to-earnings (or "P/E") ratio of 55.3x, since almost half of all companies in India have P/E ratios under 32x and even P/E's lower than 19x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so lofty.

Garden Reach Shipbuilders & Engineers certainly has been doing a good job lately as it's been growing earnings more than most other companies. It seems that many are expecting the strong earnings performance to persist, which has raised the P/E. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Check out our latest analysis for Garden Reach Shipbuilders & Engineers

What Are Growth Metrics Telling Us About The High P/E?

In order to justify its P/E ratio, Garden Reach Shipbuilders & Engineers would need to produce outstanding growth well in excess of the market.

Retrospectively, the last year delivered an exceptional 45% gain to the company's bottom line. The latest three year period has also seen an excellent 96% overall rise in EPS, aided by its short-term performance. So we can start by confirming that the company has done a great job of growing earnings over that time.

Shifting to the future, estimates from the two analysts covering the company suggest earnings should grow by 19% over the next year. That's shaping up to be materially lower than the 25% growth forecast for the broader market.

With this information, we find it concerning that Garden Reach Shipbuilders & Engineers is trading at a P/E higher than the market. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. Only the boldest would assume these prices are sustainable as this level of earnings growth is likely to weigh heavily on the share price eventually.

What We Can Learn From Garden Reach Shipbuilders & Engineers' P/E?

Even after such a strong price drop, Garden Reach Shipbuilders & Engineers' P/E still exceeds the rest of the market significantly. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

We've established that Garden Reach Shipbuilders & Engineers currently trades on a much higher than expected P/E since its forecast growth is lower than the wider market. When we see a weak earnings outlook with slower than market growth, we suspect the share price is at risk of declining, sending the high P/E lower. This places shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 2 warning signs with Garden Reach Shipbuilders & Engineers (at least 1 which is a bit unpleasant), and understanding them should be part of your investment process.

Of course, you might also be able to find a better stock than Garden Reach Shipbuilders & Engineers. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:GRSE

Garden Reach Shipbuilders & Engineers

Engages in the design and construction of war ships in India.

Excellent balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Community Narratives