These Return Metrics Don't Make Greaves Cotton (NSE:GREAVESCOT) Look Too Strong

What financial metrics can indicate to us that a company is maturing or even in decline? Typically, we'll see the trend of both return on capital employed (ROCE) declining and this usually coincides with a decreasing amount of capital employed. This indicates the company is producing less profit from its investments and its total assets are decreasing. On that note, looking into Greaves Cotton (NSE:GREAVESCOT), we weren't too upbeat about how things were going.

What is Return On Capital Employed (ROCE)?

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. The formula for this calculation on Greaves Cotton is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

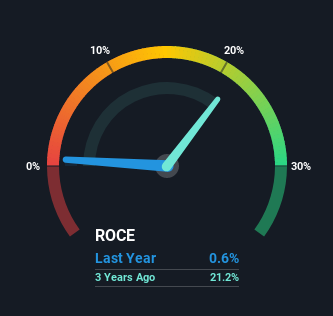

0.006 = ₹47m ÷ (₹13b - ₹4.6b) (Based on the trailing twelve months to September 2021).

Therefore, Greaves Cotton has an ROCE of 0.6%. In absolute terms, that's a low return and it also under-performs the Machinery industry average of 15%.

See our latest analysis for Greaves Cotton

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you'd like to look at how Greaves Cotton has performed in the past in other metrics, you can view this free graph of past earnings, revenue and cash flow.

What The Trend Of ROCE Can Tell Us

There is reason to be cautious about Greaves Cotton, given the returns are trending downwards. About five years ago, returns on capital were 23%, however they're now substantially lower than that as we saw above. And on the capital employed front, the business is utilizing roughly the same amount of capital as it was back then. Since returns are falling and the business has the same amount of assets employed, this can suggest it's a mature business that hasn't had much growth in the last five years. So because these trends aren't typically conducive to creating a multi-bagger, we wouldn't hold our breath on Greaves Cotton becoming one if things continue as they have.

While on the subject, we noticed that the ratio of current liabilities to total assets has risen to 37%, which has impacted the ROCE. If current liabilities hadn't increased as much as they did, the ROCE could actually be even lower. Keep an eye on this ratio, because the business could encounter some new risks if this metric gets too high.

Our Take On Greaves Cotton's ROCE

All in all, the lower returns from the same amount of capital employed aren't exactly signs of a compounding machine. But investors must be expecting an improvement of sorts because over the last five yearsthe stock has delivered a respectable 77% return. Regardless, we don't feel too comfortable with the fundamentals so we'd be steering clear of this stock for now.

If you want to know some of the risks facing Greaves Cotton we've found 2 warning signs (1 is potentially serious!) that you should be aware of before investing here.

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:GREAVESCOT

Greaves Cotton

Operates engineering and mobility retail business in India, Middle East, Africa, Southeast Asia, and internationally.

Adequate balance sheet slight.

Similar Companies

Market Insights

Community Narratives